Survey, Search & Seizure operations of the Income Tax department create a huge media spectacle. But how are these operations different from each other? What is the status of the cases filed following these operations?

The issue of ‘Black Money’ is one of the most debated topics in public forums in India. Discussions around tax havens, offshore financial hubs, shell companies dominate these debates. Multiple institutions including the Supreme Court of India, and elected representatives have unequivocally expressed concern about the growth of black money. The adverse effects of black money on a nation’s economy are very well documented, hence the growing concern of policymakers about black money.

In today’s story, we look at the different aspects of black money, the statutory processes to unearth it and some statistics related to the Income Tax searches and seizures.

Black Money and sources

Even though ‘black money’ is used in regular conversations & debates, there is no precise definition of what constitutes black money. Other connotations like ‘shadow economy’, ‘parallel economy’, and ‘dirty money’ are also used sometimes. The word ‘black money’ is not defined under the Income Tax Act, 1961; Customs Act,1962; CGST Act, 2017; and Central Excise Act, 1944. The National Institute of Public Finance and Policy (NIPFP), in its report, ‘Aspects of Black Economy in India (1985)’ defined black money as ‘aggregates of income that are taxable but not reported to tax authorities’. In simpler terms, black money is a word used in everyday speech to describe funds that are not entirely lawful in the owner’s possession. However, black money may also mean money that is earned through illegal means.

There are three primary sources of black money- Crime, Corruption and Business. The first source, ‘crime’, is the money that might have come from illegal acts that are against the law, such as crime, drug trafficking, sexual exploitation and trafficking, bank fraud, and terrorism, all of which are punishable by the state’s legal system. The ‘corruption’ component includes the money received by graft or bribery, and siphoning public money by leakages, among others. The ‘business’ component could be in the most common process of tax evasion using shell companies, tax havens, and under-disclosing of incomes and expenditures. It is important to understand that in the first two sources, ‘crime’ and ‘corruption’, black money is generated through legally non-permissible activity while in the ‘business’ component, the activity is legally permissible. A large share of black money is through the ‘business’ component.

Tackling unaccounted/black money

Successive governments have been trying to minimize, if not eradicate the menace of black money through various means- using legislations, capacity expansions and plugging the existing loopholes. The Income Tax Department is primarily responsible for fighting the threat of black money. To accomplish the goal of deterring tax evasion, it employs the tools of scrutiny assessment as well as information-based investigations to identify tax evasion and punish it in accordance with Income Tax Act regulations. Further, The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (BMA, 2015), which came into effect on 01 July 2015, is a new, comprehensive law that imposes strict penalties. The BMA, 2015’s one-time three-month compliance window, which ended on 30 September 2015, saw 648 declarations regarding undeclared foreign assets valued Rs. 4164 crores. Over Rs. 2476 crores in such cases was collected as tax and penalties.

According to the Prevention of Money Laundering Act, 2002 (PMLA), the offence of wilful attempt to evade tax, etc. in relation to undeclared foreign income/assets is a Scheduled Offense, for which the Directorate of Enforcement (ED) takes the appropriate action, including identification of the proceeds of crime generated, provisional attachments, and filing of prosecution complaints in appropriate cases. Proceeds of crime of Rs. 42.57 crores have been attached or seized throughout the course of the investigation in 13 PMLA cases including predicate offences involving BMA, 2015 violations, and three prosecution reports have been made. Also, under section 37A of the FEMA, assets worth Rs. 93.07 crores have been taken in 05 cases.

Among all the strategies, income tax ‘search and seizures’ is the most commonly adopted strategy to unearth undisclosed incomes or detect tax evasions. The investigation wing of the IT department deals with investigations to detect tax evasions and carries out operations such as ‘surveys’, ‘search and seizures’ to gather evidence of such unauthorized tax evasions.

Income tax ‘raids’- Types and differences

Though used commonly by media and the public at large, the Income Tax Act, 1961 does not mention the word ‘raid’. However, as mentioned earlier, the income tax department is equipped with powers under the IT Act, 1961 to conduct search and seizure operations.

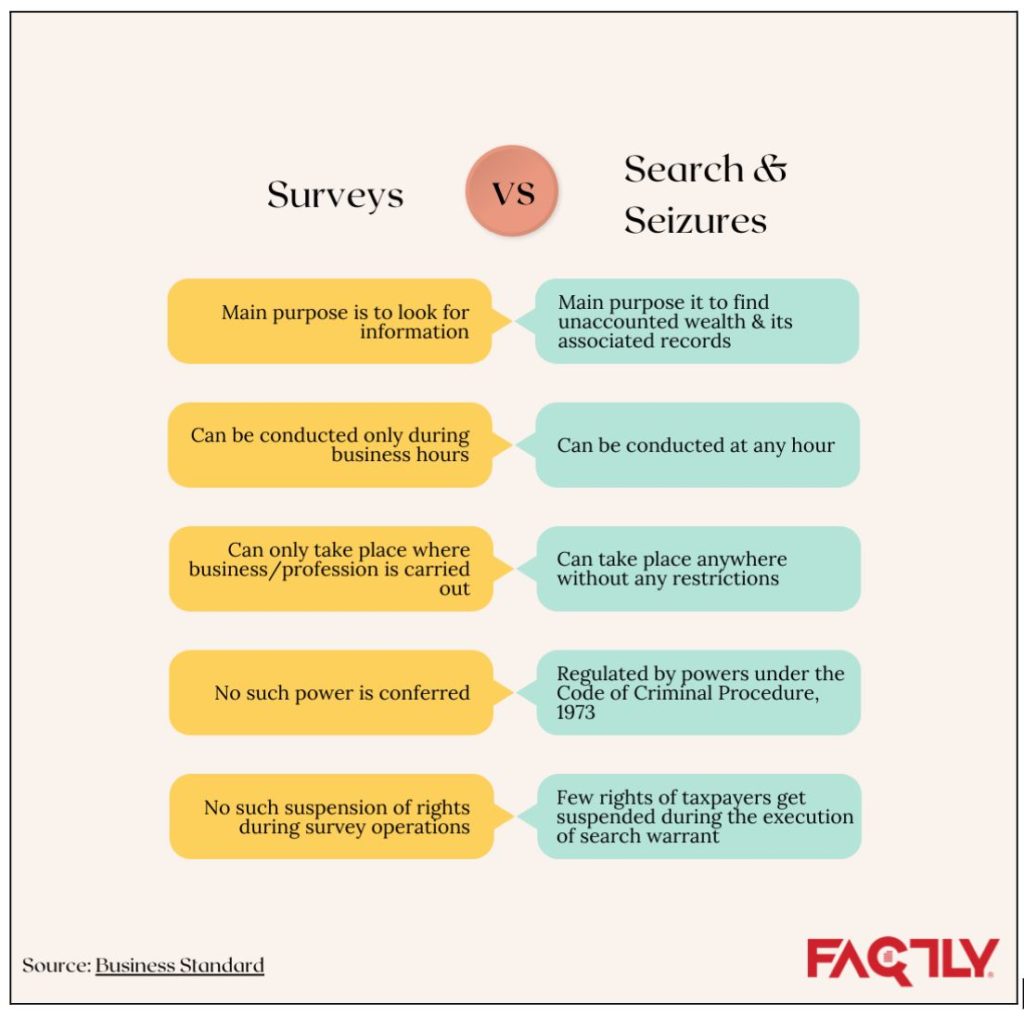

Section 132 (1) of the Income Tax Act, 1961, authorizes the officers to carry out search and seizure operations. Surveys are carried out under Sections 133(A)(1), 133(A)(5), and 133(B). Usually, all types of surveys, searches and seizures are mentioned under the umbrella term ‘raid’. However, there is a difference between them as explained below.

The aftermath of ‘survey’ and ‘search and seizure’ operations

The Manual of Office Procedure provides for the procedures to be followed while conducting any operations of survey, search and seizure. As mentioned earlier, surveys are carried out under sections 133(A)(1), 133(A)(5) and 133(B) of the Income Tax Act, 1961. After the survey is completed, a self-contained report for surveys under any section shall be prepared about the operation and result of the survey, which has details including, name and assessee, details of PAN, the purpose of the survey, a brief narration of work done and material found during the survey, details of statements recorded, among others. In addition,

- For the survey under section 133(A)(1), the time and date of entry into the premises surveyed and the time of conclusion of the survey, surveying authority’s comments, including comments on the follow-up action required, list of books of account and other documents impounded and retained in his custody by the income-tax authority and the date on which this was done, details of cash/ stock found, discrepancy, if noticed and reconciliation or explanation given by the person present and details of other significant transactions noticed among others are recorded.

- For surveys under section 133(A)(5), The Directors-General of Income-tax (Inv.). should, in appropriate cases, issue press releases giving broad details of the results achieved, without mentioning the names of the persons covered in the survey u/s 133 (A)(5). No name of any officials should be mentioned in any press release. For instance, here is the press release issued following the survey operations at BBC premises in Delhi & Mumbai.

- For surveys under section 133B, the Inspector who conducted the survey should give a brief supplementary report, among others estimating the income of the person, if such estimate varies substantially from the estimate given by the person in Form No. 45D. The Inspector who conducted the survey should also give the basis for such estimate and the recommendation for follow-up actions, such as those u/s 142/147, especially in the cases of new taxpayers.

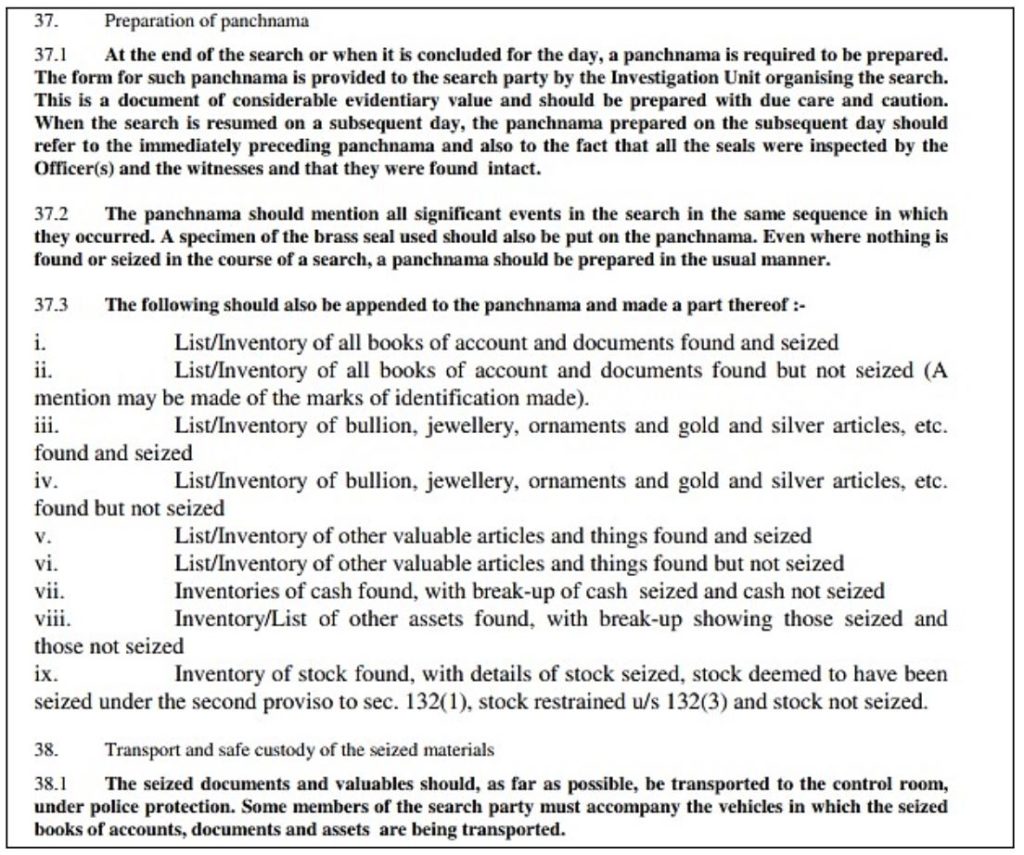

For ‘searches’ and ‘seizures’, a panchnama is prepared at the end of each day of such search.

Further, the search party shall prepare a report.

Trend in search & seizure actions conducted by the Income Tax Department

The data from the parliamentary responses indicate that in there is no uniform trend that can be observed in the number of search and seizure operations and the value of assets seized. However, the year 2016-17 registered a higher number of searches and seizures. The demonetization and the aftermath could probably be the reason behind such high numbers. The value of assets seized is highest in 2018-19 with Rs. 1567 crores, followed by Rs. 1470 crores in 2016-17.

Huge pendency in search & seizure cases

Income Tax searches and seizures create a huge uproar in the media and the public at large. Allegations and counter-allegations are levelled. However, the end outcomes of such operations are rarely spoken about. The data of the prosecutions launched by the department and the convictions indicate abysmal performance in the further stages of the investigation. There is a huge pendency in the search and seizure cases, and with the addition of new cases in which prosecution is launched every year, this pendency is expected to only grow.