The Reserve Bank of India (RBI) recently released its Payments Vision 2025, with a key focus on strengthening the e-payments ecosystem in India. This current vision document builds on the Payments Vision 2019-21 document and provides an outline of the initiatives and expected outcomes by the end of 2025.

The Reserve Bank of India (RBI) recently released its Payments Vision 2025, with a key focus on strengthening the e-payments ecosystem in India. This current vision document builds on the Payments Vision 2019-21 document and provides an outline of the initiatives and expected outcomes by the end of 2025. In continuation of the targets set earlier, the ‘Payments Vision 2025’ document aims at achieving more than 3 times increase in digital transactions by 2025. Here’s a review of this vision document.

Providing affordable, secure, and accessible e-payments is a key part of Payments Vision 2025

The payment systems in India have undergone a remarkable transformation over the years. RBI’s Payment Vision 2025 aims at pushing the envelope further to elevate the payment systems to empower users with affordable payment options that are conveniently accessible anytime and anywhere.

This involves an expansion of reliable digital payment options, which is highlighted in the vision document’s theme of “ E-Payments for Everyone, Everywhere, Everytime (4 Es)” .

The vision document entails 5 Goals – Integrity, Inclusion, Innovation, Institutionalisation & Internationalisation, which influence the various initiatives and the expected outcomes that are outlined in the vision document.

The vision document notes that there is a change in the customer behaviour in embracing digital and touchless modes of payments, with COVID-19 pandemic playing a role in this change. There is an estimated 50% increase in mobile banking users with many of them being first-time users. One of the key challenges that this vision document envisages addressing is making this an irreversible shift.

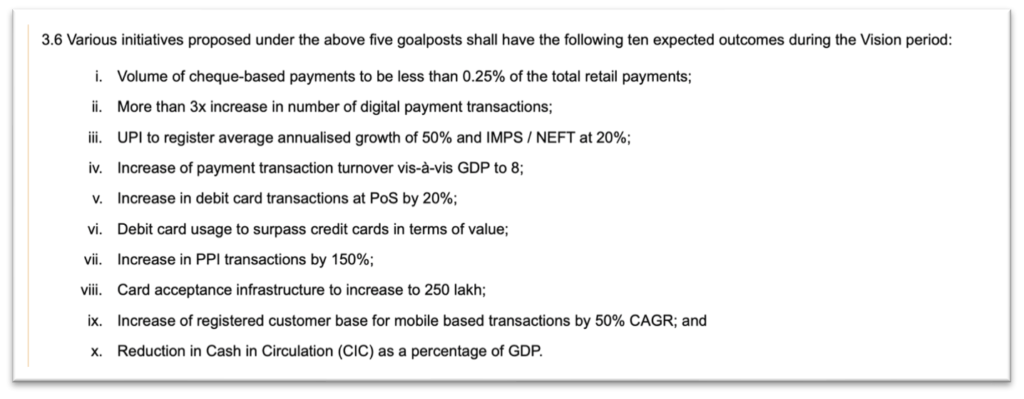

Increase in Digital & PPI transactions and reduction in usage of cash among the expected outcomes

The ‘Payments Vision 2025’ document specifies 10 expected outcomes which act as measurables for the various initiatives that are proposed under the five goals mentioned earlier.

These 10 expected outcomes can be broadly classified as achieving two purposes – to reduce the reliance on cash and to increase the usage of various modes of digital payments.

As highlighted earlier, one of the key expected outcomes by 2025 is to increase the number of digital payment transactions by more than three times. In 2021-22, there were a total of 8.84 thousand crores digital payment transactions, compared to 5.55 thousand crores in 2020-21, i.e. an increase of about 60%.

The expected outcome for UPI payments is to increase at an annualised growth of 50%, while in the case of IMPS/NEFT transactions, it is 20%. The vision document lists expected outcomes for other payment options like debit & credit cards. One of the targets is to make efforts to increase debit card transactions compared to that of credit card transactions, which could mitigate the risk of bad debts. The expected outcome is to increase the debit card transaction usage at PoS by 20%.

Two of these expected outcomes are related to reduction in reliance on traditional payment options. It is targeted to have the volume of cheque-based payments to be less 0.25% of the total retail payments. Another outcome is to reduce the Cash in Circulation (CIC) as a percentage of GDP. Our story relating to this can be read here.

As indicated earlier, there has been an increase in the number of new users for digital payments over the past couple of years. One of the intended outcomes of ‘Payments Vision 2025’ is to increase the registered customer base for mobile-based transactions by 50% CAGR.

Among the various initiatives outlined in the vision document are to increase the digital payment options in not only the smart phones but also the feature phones. Involving big tech companies and encouraging innovation are expected to pave way for solutions to meet these targets.

Fourfold increase in the number of digital transactions among the expected outcomes of the previous vision document.

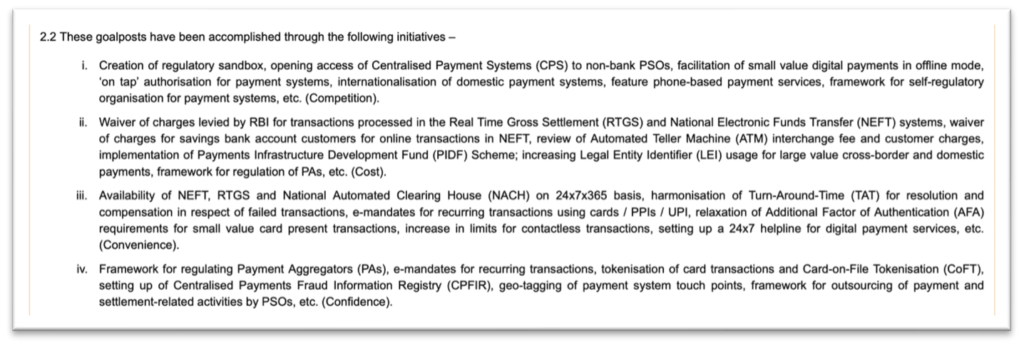

‘Payments Vision 2025’ is expected to further the agenda envisaged under ‘Payments Vision 2021’, the vision of which was to empower every Indian with access to a bouquet of e-payment options. There were four goals set by Vision 2021 – Competition, Cost, Convenience, and Confidence.

The action points in the document are envisioned to deliver on 12 expected outcomes. One of the expected outcomes is to increase the number of digital transactions by four times between 2018-2021 i.e., to around 8.7 thousand crore transactions by end of 2021. As indicated earlier, there were a total of 8.84 thousand crore transactions for 2021-22. The volume of BHIM UPI transactions has also increased from 535 crores in 2018-19 to 4.5 thousand crores in 2021-22.

The adoption of digital modes for payments was one of the important outcomes for the initiatives envisaged in Vision document 2021. RBI stated that there is a 500% increase in the number of merchants accepting digital modes of payment by the end of September 2021, compared to half-year ending March 2019.

During the same period, the number of unique users of mobile banking has increased by 99% and that of internet banking has increased by 18%.

On the other hand, there was also a drop in the usage of paper instruments for retail transactions from 3.83% to 0.8% in terms of volume. However, one expected outcome which was not met by end of 2021, was the increase in the usage of Debit cards for payment transactions, especially at PoS. The lockdown measures due to the COVID-19 pandemic could be a major reason for the same. In 2019-20, 512 crores transactions were done through debit cards, while in the ensuing two years, it was 411 crores and 394 crores respectively. Meanwhile, there is an increase in Credit card transactions in 2021-22 after the low in 2020-21.

In its statement along with the release of ‘Payment Vision 2025’ document, RBI highlighted the initiatives which contributed towards achieving the goals of ‘Vision 2021’. These include – waiver of charges for online transactions, 24x7X365 availability of NEFT, RTGS and National Automated Clearing House (NACH), framework for regulating payment aggregators, setting up of Centralised Payments Fraud Information Registry (CPIFR), etc among others.

Stabilising & Securing payment systems along with increasing the scope of initiatives

Apart from listing the expected outcomes for ‘Payments Vision 2025’, the RBI laid out the plan for various initiatives which could contribute to achieving the outcomes. There are 47 specific initiatives outlined under the 5 goal posts of 5I i.e. Integrity, Inclusion, Innovation, Institutionalisation & Internationalisation.

Some of the highlights among these initiatives include :

- Regulation of payment intermediaries and online payment aggregators and to get all of them under the ambit of RBI.

- Cognizance of the costs involved in providing digital payment services and review these digital costs, to ensure that the burden of these costs does not impact the adoption of digital payment systems.

- Review the different types of PPIs (Prepaid Payment Instruments) and issue relevant guidelines to ensure the security of the transactions.

- Emphasis on building authentication mechanisms for payment transactions by leveraging behavioural biometrics, location, historical payments, etc. to provide safer and transparent payment solutions.

- Global outreach of UPI as part of Internationalization goal.