The RBI released the 21st issue of the ‘Financial Stability Report recently. Among other things, the report addressed the issue of payment & settlement systems and mentioned three important initiatives aimed at encouraging non-cash transactions. Here is a review.

The Reserve Bank of India (RBI) released the 21st issue of its bi-annual report- the Financial Stability Report (FSR), in July 2020. The purpose of this report is to ascertain the financial stability of the economy by reviewing the potential risks and their impact on the various components of the economy. It also provides insights into the measures taken and the proposed plans by RBI and other authorities to handle these risks and mitigate any negative impact of them on the economy.

The current report takes prominence as it is released amidst the gloomy economic situation due to the COVID-19 pandemic. The economy is currently under severe stress due to the lockdown imposed across the country few months ago as well as the challenges faced as part of unlock process.

In an earlier story, we looked into what this report has to say about the health of Banks in the country. In this story, we look into the initiatives being taken and proposed by RBI regarding Payments & Settlements. With people opting for limited movement, online payments have become important for financial transactions and play a key role in the efforts to revive the economy amidst this gloomy situation.

The FSR provides information about three measures taken by RBI since December 2019 in regards to Payment & Settlement Systems.

- Launch of NEFT – 24x7x365

- Business Continuity of Payment Systems

- Setting up the Payments Infrastructure Development Fund

Round-the-Clock transfer availability under NEFT

National Electronic Fund Transfer (NEFT) is an RBI operated nation-wide centralized payment system. This enables bank customers in India to transfer funds between any two NEFT enabled bank accounts.

As per the RBI’s Annual Report for 2018-19, transactions worth ₹ 228 lakh crores were done through NEFT during 2018-19. This is nearly double the value, two years ago i.e. ₹ 120 lakh crores in 2016-17. The total number of NEFT transactions in 2018-19 were around 232 crores.

Comparatively, the total value of amount transferred through IMPS was nearly ₹ 16 lakh crores from 175 crore transactions. This indicates that NEFT is the preferred option for higher volume transactions, due to the monetary limits on IMPS transactions.

However, a main drawback of the NEFT system was with the limitations around the timings. Earlier, an NEFT transaction could only be done between 8:00 AM to 7:00 PM. Furthermore, NEFT can be done only on working days i.e. all the public holidays along with 2nd & 4th Saturdays where in the banks are closed, an NEFT transactions could not be done.

Effective from 16 December 2019, RBI has announced that the NEFT transactions can be done round the clock and across all the days in a year. This provides the feasibility of transferring funds, making utility payments, making purchases etc. round the clock. The RBI issued a circular to this effect on 06 December 2019 about the new NEFT system.

With this, India joins an elite group of five other countries – United Kingdom, Hong Kong, South Korea, Singapore and China to provide round-the-clock fund transfer facility. This initiative was driven as part of ‘Payment and Settlement Systems in India: Vision – 2019-2021’ released in May 2019.

Round the clock availability of NEFT without the dependence on working of the banks was a great advantage during the lockdown. The impact of this in terms of volume and value of the transactions can be ascertained once RBI divulges the details.

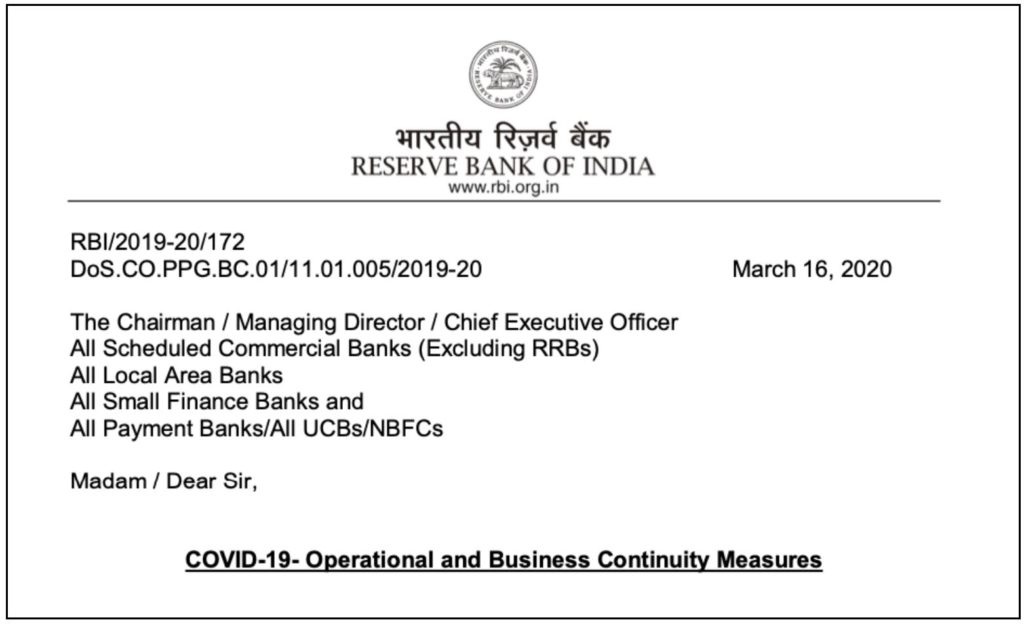

Ensuring Business Continuity during COVID-19 Lockdown

RBI has a Business Contingency Plan (BCP) in place, to be implemented in case of any emergencies and contingencies. COVID-19 was one such emergency which prompted the implementation of BCP. Accordingly, RBI alerted the different stakeholders of the Banking System India and initiated the Business continuity measures on 16 March 2020.

Ensuing that payment systems run smoothly without being impacted by lockdown and other COVID-19 measures were a key part of the Business Contingency Plan rolled out by RBI. As per the update provided in FSR, the following initiatives were taken by RBI for smooth running of payment systems.

- Day-to-day operations of RTGS (Real Time Gross Settlement) & NEFT systems were shifted to Primary Data Centre, under protected environment.

- Work-from-home procedures were implemented by Clearing Corporation of India Limited (CCIL) for its officials. CCIL takes care of financial market infrastructure for Money market, government securities & foreign exchange settlements.

- Skeletal staff was maintained in the office of CCIL along with minimum staff in remote disaster recovery sites, for them to take over in case of any disruptions in the primary sites.

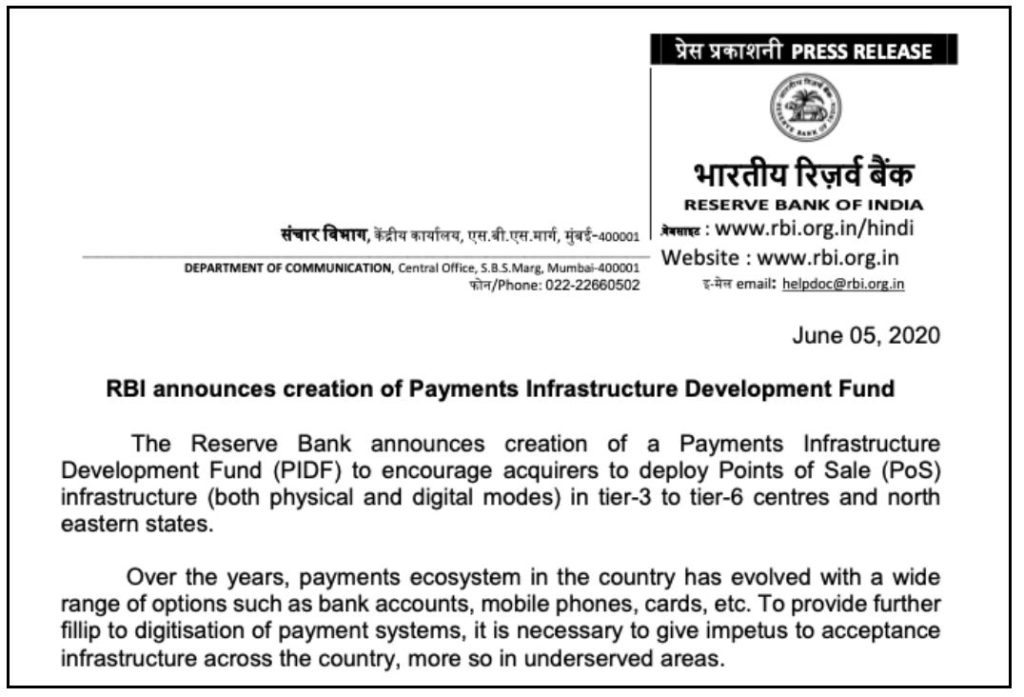

Setting up of Payments Infrastructure Development Fund

As per RBI’s annual report for 2018-19, the total number of transactions at Point of Sale (PoS) Terminals during 2018-19, using Credit cards was around 176 crores, while that of transactions through Debit Cards and PPIs (Pre-paid Payment Instruments) were 440 crores and 460 crores respectively.

Meanwhile, there was also an increase in the ‘Acceptance Infrastructure’ i.e. the equipment which is used to accept the cards for payment. The number of PoS terminals increased from 30.8 lakhs as on 31 March 2018 to 37.2 lakhs by 31 March 2019, an increase of 21%. During the same period, the number of ATMs declined by more than 500.

Creating an ‘Acceptance Development Fund’ was part of Payments Systems Vision 2019-21.

Accordingly, RBI created a Payments Infrastructure Development Fund (PIDF) on 05 June 2020, to subsidise the deployment of PoS acceptance infrastructure. The main emphasis of this fund is to increase the infrastructure in Tier-III to Tier-VI centres along with north-eastern parts of India.

RBI made an initial contribution of ₹ 250 crores towards the corpus of the fund. This covers half of the fund, with the remaining contribution coming from card issuing banks and Card networks operating in the country. The fund would be governed by an Advisory Council, which is managed and administered by RBI.

Efforts towards hassle-free payment transactions

The spur in the number of UPI transactions in 2018-19, to the tune of 535 crores compared to around 92 crores in 2017-18, raises important questions on the rationale of investing in PoS infrastructure rather than encouraging non-cash, non-card transactions, especially in times of limited public movement & social distancing norms due of COVID-19. However, considering the fact that the focus of the fund would be to encourage the cashless transactions in Tier-III and lower centres, this may encourage noncash transactions in these places. The efficacy will only be known once the data is available.

The initiative to make NEFT available round the clock is also a positive step aimed at removing hurdles in online transactions in terms of time-limitations etc.

While there has been a general slowdown in the economy and hence decline in spending, considerable number of online transactions have taken place during the lock down, which RBI has so far managed to handle effectively without any hiccups. The Annual Report for 2019-20 and later years together with other details from RBI on the volume of online transactions would throw more light on the effect of COVID-19 on the payments & settlement transactions.

Featured Image: RBI’s Financial Stability Report