In this roundup of court judgements, we look at Constitutional Courts’ remarks & directions about exclusion criteria of pre-existing illness in medical insurance, Centre’s affidavit to Supreme Court on EWS Reservation, and Karnataka high court’s rules on live-streaming and recording of court proceedings. Gujarat high court has emphasised that no person or court can force a wife to cohabit and establish conjugal rights.

Supreme Court: If the insured suffers a sudden sickness that is not expressly excluded under the policy, the insurer is to indemnify the expenses incurred.

In the case Manmohan Nanda vs. United India Insurance Co. Ltd., the Supreme Court held that if the insured suffers a sudden sickness or ailment which is not expressly excluded under the policy, a duty is cast on the insurer to indemnify the appellant for the expenses incurred.

The apex court was hearing an appeal filed by the petitioner challenging the order (dated 22 May 2015) passed by the National Consumer Disputes Redressal Commission related to Consumer Complaint No. 92/2010.

The appellant sought an overseas mediclaim policy for his intended travel to the USA. The appellant was medically examined, and the report categorically noted that the appellant had diabetes type II (also known as diabetes mellitus) and no other adverse medical condition was found. In the medical examination report, a specific query was sought as to whether any abnormalities were observed in the electrocardiogram test of the appellant. There was another query regarding any possible illness or disease for which the appellant may require medical treatment in the ensuing trip to the USA. To both these queries, the doctor who examined the appellant had answered “normal” and “no” respectively.

Thereafter, the Overseas Mediclaim Business and Holiday Policy was issued, which was valid from 19 May 2009 to 01 June 2009 for the appellant. Upon reaching San Francisco on 19 May 2009, the appellant felt weak and started sweating. Initially, his wife got him admitted at the SFO Medical Centre at San Francisco airport and later he was shifted to the Mills-Peninsula Medical Centre where angioplasty was performed on 19 May 2009 and 22 May 2009 and three stents were inserted to remove the blockage from the heart vessels.

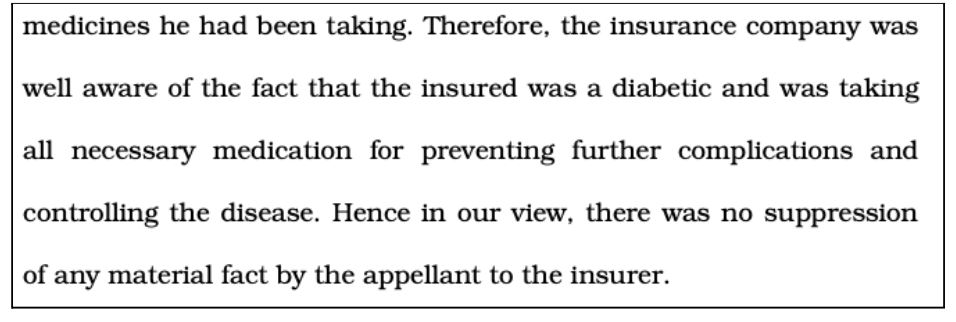

On 19 August 2009, the appellant sent a letter annexing all bills in original as well as the discharge summary to the Divisional Manager of the Insurance Company (United India Insurance) at their Bhopal office. On 22 August 2009, the appellant received a letter stating that his claim had been repudiated as the appellant had a history of hyperlipidaemia and diabetes and the policy did not cover pre-existing conditions and complications arising therefrom. The said repudiation was regarding the bill raised by the Medical Centre for USD 2,29,719.

Being aggrieved, the appellant filed a complaint under Section 21 (9) of the Consumer Protection Act, 1986 (Consumer Complaint No.92/2010). A reply was filed by the Insurance company arguing that the claim was rightly rejected on the ground of nondisclosure of a pre-existing disease as the treatment report of the appellant showed prior medication such as statins, which is a lipid-lowering medicine. To this, the appellant also filed an additional affidavit enclosing the medical opinions of three doctors on affidavit stating that prescription of statins to a person having diabetes type II is by way of precaution and not because the patient would be suffering from any cardiovascular disease.

Subsequently, the National Consumer Disputes Redressal Commission dismissed the complaint filed by the appellant on the ground of nondisclosure of material facts.

Therefore, in this appeal before the apex court, the appellant has contended that there was no intention to suppress any material fact as the appellant had no knowledge that he was suffering from hyperlipidaemia as on 15 May 2009, when the proposal form was filled by him. The appellant stated that the same was diagnosed for the first time on 19 May 2009, at the Medical Centre in San Francisco. The obligation to disclose any fact extends only when the said fact is known to the appellant but not otherwise.

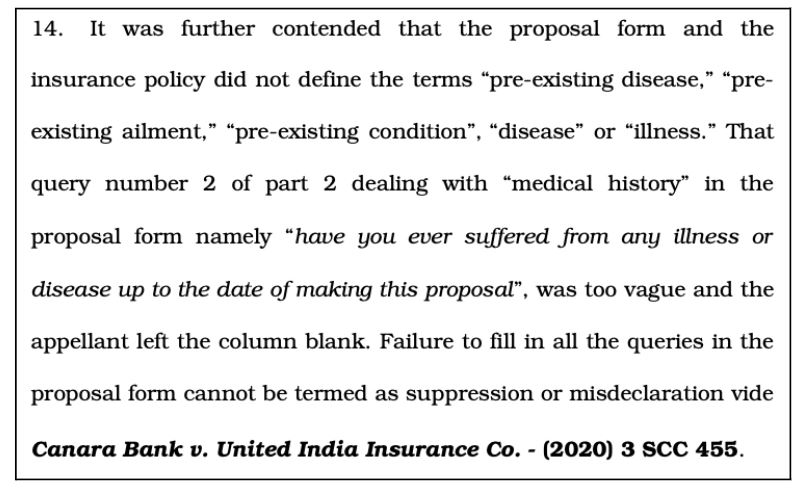

Further, it was submitted that question number 5 which read, “Have you ever suffered from any illness or disease or had any accident prior to the first day of insurance” is also overarching as no person can answer such a question in the negative. Every person to whom a mediclaim policy is offered would have, at some point of time, suffered from some disease or illness but for the same to be considered as pre-existing disease, ailment, condition, or illness on which ground a claim could be repudiated, there is need for a specific definition to be incorporated in the policy.

Therefore, the counsel for the appellant submitted that for an insurer to repudiate the policy it must establish suppression or misrepresentation of material facts on the part of the insured. In this instance, the insurance company was also required to prove the following:

- That the heart attack suffered by the appellant on 19 May 2009, was caused by diabetes mellitus type II and hyperlipidaemia,

- That hyperlipidaemia was a “pre-existing condition”

- That this fact was known to the appellant and was suppressed by him at the time of filling up the proposal form, i.e., on 15 May 2009.

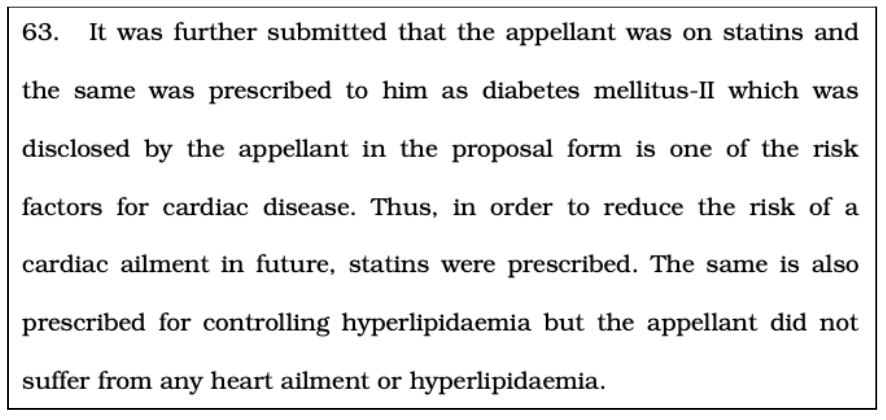

The apex court noted that there is considerable force in the argument made on behalf of the appellant. The appellant only had knowledge of diabetes mellitus II, for which he was under treatment. To disclose the status of the said disease he had submitted his ECG report, blood and urine test reports which showed normal results – indicating that the appellant had no cardiac disease.

Therefore, the bench noted that the prescription of statins to the appellant was only as a precaution to prevent a possible cardiac ailment from developing in the future as diabetes mellitus II is a risk factor for such a disease. But by that, it cannot be deduced or inferred that because the appellant had a cardiac ailment or hyperlipidaemia, he was prescribed statins.

In conclusion, the bench held that the respondent insurance company could not have repudiated the policy on the ground that acute myocardial infraction suffered by the appellant on landing at San Francisco, USA was a “pre-existing and related complication” which was excluded under the policy.

Therefore, the apex court held that the repudiation of the policy by the respondent insurance company is illegal and not in accordance with the law. Consequently, the appellant is entitled to be indemnified under the policy. The respondents have been directed to indemnify the appellant regarding the expenses incurred towards his medical treatment within a period of one month with interest at the rate of 6% per annum from the date of filing the claim petition before the Commission till realisation.

Centre Tells Supreme Court: EWS Reservation – No Change in Rs 8 Lakhs Gross Annual Income Cut-Off; Residential Asset Criteria Omitted

In response to a writ petition challenging the Centre’s decision to introduce ‘Economically Weaker Section (EWS)’ reservation in the All-India Quota for NEET, the Central Government submitted an affidavit highlighting that it has decided to accept the recommendation made by an expert committee to retain the limit of INR 8 lakh gross annual income for EWS reservations.

The Centre has also accepted the recommendation to omit the residential asset criteria for EWS eligibility. However, the ongoing admissions, including the NEET-PG counselling, will proceed as per the existing criteria and the revised criteria will be applied from the next academic year onwards.

After the Supreme Court expressed doubts regarding the reasonableness of INR 8 lakh income criteria for EWS, the Centre agreed to revisit the same after formulating an expert committee. On 30 November 2021, the Committee was formed comprising Ajay Bhusan Pandey (Former Finance Secretary, GoI), Prof VK Malhotra (Member Secretary, ICSSR), and Sanjeev Sanyal (Principal Economic Advisor to GoI).

As per the existing guidelines, persons who are not covered under the scheme of reservation for SCs, STs and OBCs and whose family has a gross annual income below INR 8 lakh are to be identified as EWSs for benefit of reservation. Income also had to include income from all sources i.e., salary, agriculture, business, profession etc. for the financial year prior to the year of application. Furthermore, persons whose family owns or possesses any of the following assets were to be excluded from being identified as EWS:

- five acres of agricultural land and above.

- a residential plot of 100 square yards and above in notified municipalities and 200 square yards and above in areas other than notified municipalities; and

- a residential flat of 1000 square feet and above

As per the revised guidelines, the Centre has accepted the Committee’s recommendation to omit the residential asset criteria. The affidavit provides clarification for the specific cut-off at INR 8 lakh for the EWS category, as it is the same as OBC creamy layer cut-off. The Supreme Court had prima facie observed that applying the income limit criteria (INR 8 lakh annual income) of OBC Creamy lawyer to EWS was unreasonable, as the latter had no concept of social and economic backwardness.

In this regard, the union government’s affidavit provided the following explanation:

- EWS’s criteria are related to the financial year prior to the year of application whereas the income criterion for the creamy layer in the OBC category is applicable to gross annual income for three consecutive years.

- For deciding the OBC creamy layer, income from salaries, agriculture and traditional artisanal professions was excluded from the consideration whereas INR 8 lakh criteria for EWS included that from all sources including farming.

Karnataka HC notifies rules on live-streaming and recording of court proceedings.

The Karnataka High Court has notified the Karnataka Rules on Live Streaming and Recording of Court Proceedings, 2021, which came into force from 01 January 2022, and apply to the High Court and to courts and tribunals over which it has supervisory jurisdiction.

The guidelines are designed to lay down the practice and procedure to be followed to imbue greater transparency, inclusivity, and foster access to justice. As per the notified rules, “Live-stream or Live-streamed or Live-streaming” means and includes a live television link, webcast, audio-video transmissions via electronic means or other arrangements whereby any person can view the Proceedings as permitted. “Proceedings” means and includes judicial proceedings, administrative proceedings, Lok Adalat proceedings, full-court references, farewells and other meetings and events organised by the Court.

All proceedings will be live-streamed by the Court; however, the following will be excluded:

- Matrimonial matters, including transfer petitions

- Cases concerning sexual offences, including proceedings instituted under section 376, Indian Penal Code, 1860.

- Cases concerning gender-based violence against women.

- Matters registered under or involving the Protection of Children from Sexual Offences Act, 2012 (POCSO) and under the Juvenile Justice (Care and Protection of Children) Act, 2015.

- In-camera proceedings as defined under Section 327 of the Code of Criminal Procedure, 1973 (CrPC) or Section 153 B of the Code of Civil Procedure, 1908.

- Matters where the Bench is of the view, for reasons to be recorded in writing, that publication would be antithetical to the administration of justice.

- Cases, which in the opinion of the Bench, may provoke enmity amongst communities likely to result in a breach of law and order.

- Recording of evidence, including cross-examination.

- Privileged communications between the parties and their advocates; cases where a claim of privilege is accepted by the Court; and non-public discussions between advocates.

- Any other matter in which a specific direction is issued by the Bench or the Chief Justice.

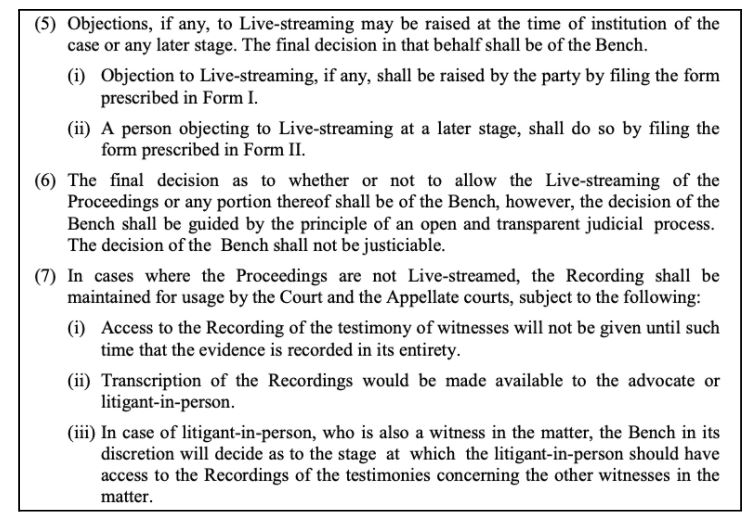

The guidelines also specify the procedure for raising objections to live-streaming, and the procedure to be followed where the proceedings are not live-streamed.

The anonymity of the victims and witnesses is to be maintained in the recordings via dummy names, face-masking, pixelation and/or electronic distortion of voice, as and when directed by the Court. As per the guidelines, any audio-video recording or recording of proceedings by any other means, beyond the mandate of the present Rules is expressly prohibited. Rules for storage, transcription, and access have also been notified.

Gujarat HC: Muslim husband has no fundamental right to compel the wife to share his consortium with another woman.

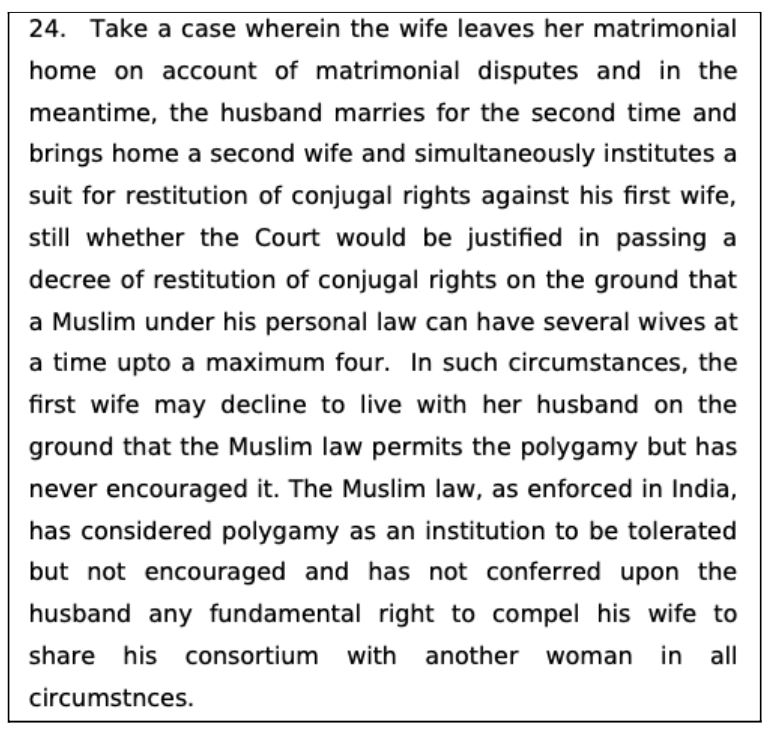

In the case Jinnat Fatma Vajirbhai Ami w/o Nishat Alimadbhai Polra v. Nishat Alimadbhai Polra, the Gujarat high court held that as per Muslim law, as enforced in India, a husband has not been given any fundamental right to compel his wife to share his consortium with another woman (husband’s other wives or otherwise) in all circumstances.

The high court was hearing a plea filed by Jinnat Fatima challenging the Family court (Banaskantha district in Gujarat) decision that had directed her to go back to her matrimonial home and perform conjugal obligations. In a suit filed by the husband for restitution of conjugal rights, the Banaskantha family court allowed the suit filed by the husband and directed his wife to go back to her matrimonial home and perform conjugal obligations.

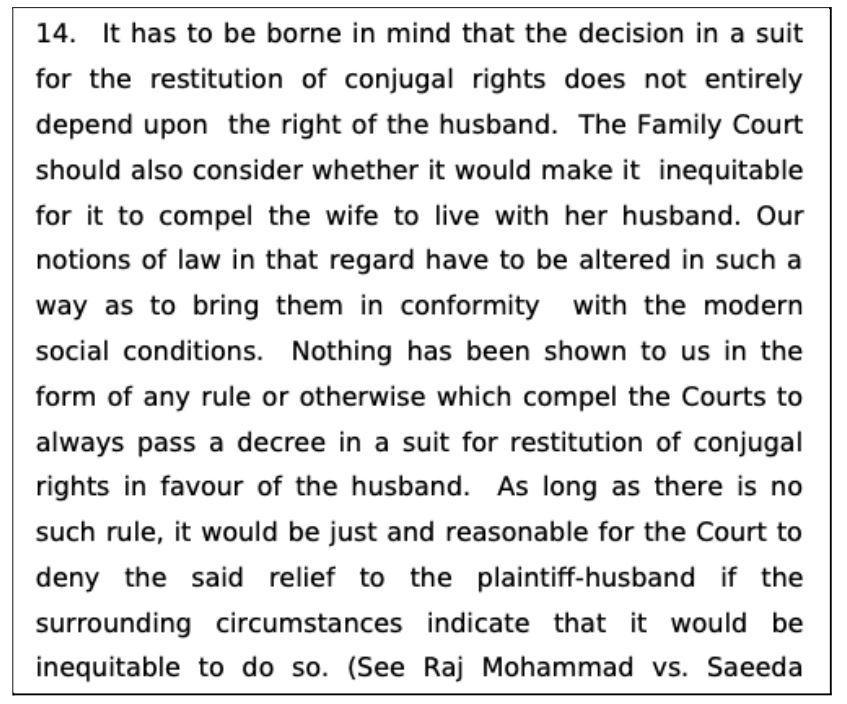

At the outset, the high court observed that the decision for the restitution of conjugal rights does not entirely depend upon the right of the husband and that the Family Court should also consider whether it would make it inequitable by compelling the wife to live with her husband.

Overturning the family court’s order, the high court held that no person or court can force a wife to cohabit and establish conjugal rights. If the wife refuses to cohabit, she cannot be forced by a decree in a suit to establish conjugal rights.

The bench of Justice J. B. Pardiwala and Justice Niral Mehta made a significant observation vis-à-vis the Muslim law. The bench emphasized that Muslim law does not encourage polygamy as an institution, but only tolerates the same and therefore, the first wife of a Muslim husband can decline to live with her husband (who has married another woman).

Featured Image: Important Court Judgements