The issue of tax exemption to ‘Agricultural Income’ has been contentious and debated for decades now. Multiple committees highlighted the misuse of exemption in their reports. Here is a review.

The exemption of agriculture income from tax without any limit has often been pointed out as being a conduit for avoiding taxes and money laundering, which hinders the growth of the agriculture sector on which a major chunk of the Indian population is dependent on. It has often been reported that rich farmers with large landholdings and companies making profits of crores of rupees are exempted from paying tax as per the existing legal provisions. Despite this being highlighted for many decades in government reports, by lawmakers, and research papers, successive governments have not taken any action to bring agricultural income into the tax net, making it a political issue.

What is Agriculture income as defined in the Income Tax Act?

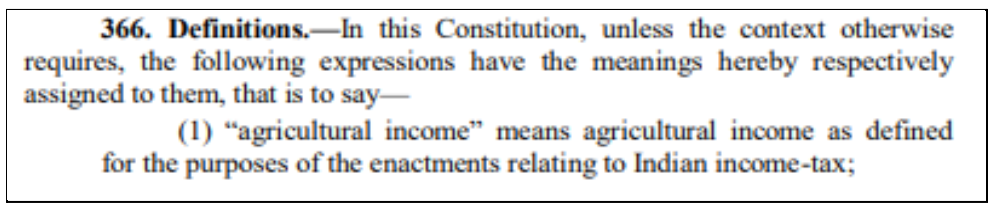

‘Agricultural income’ in the Constitution refers to that as defined for the purpose of enactments relating to Indian Income Tax according to Section 366(1) of the Constitution.

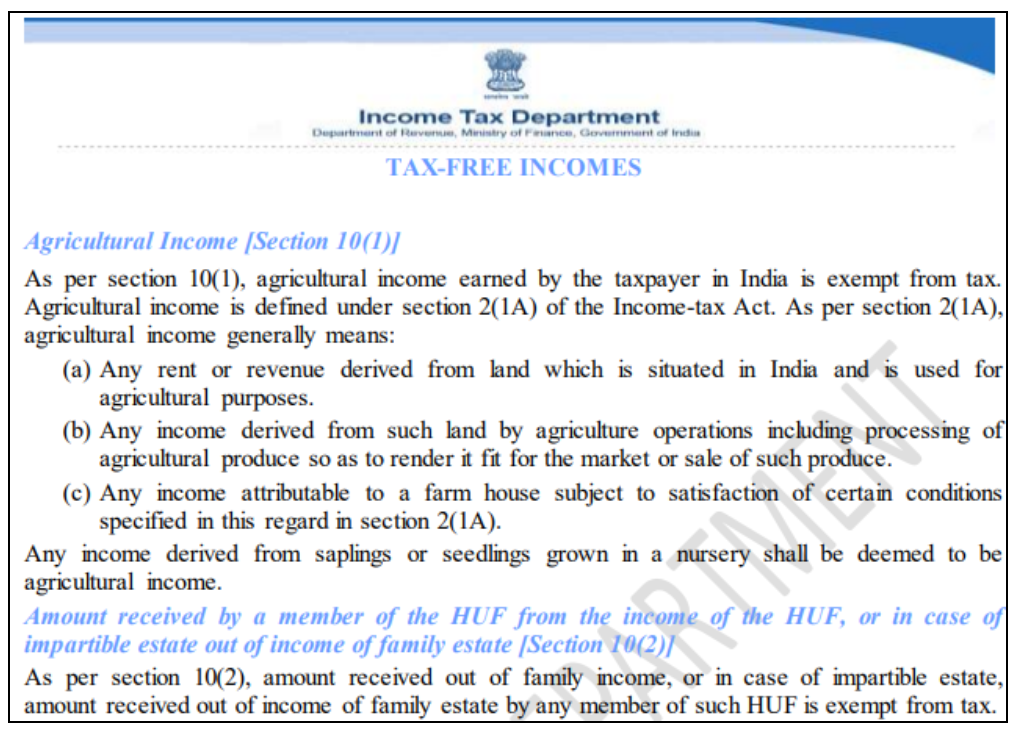

Section 2(1A) of the Income Tax Act defines agriculture income as rent/revenue from agricultural land, agricultural operations, or farmhouse. Section 10(1) of the Act exempts agriculture income from tax.

Taxes on agricultural income falls under the ambit of the “State” as per the Constitution of India which means that enactment of legislations pertaining to taxing agriculture income is the responsibility of State Governments and not the Central Government. Taxes on agricultural income is part of the ‘State List’ under the seventh schedule of the constitution. Nonetheless, agricultural income is used for rate purposes under certain conditions to determine income tax liabilities.

Numerous official reports have highlighted the misuse of agricultural income tax exemption for decades

Though the exemption was granted to support farmers improve their conditions, the provision is being misused widely as noted in multiple reports in the past. The same has been highlighted in numerous government reports as well.

The Taxation Enquiry Committee in 1924-25 has discussed the issue of tax exemption of agriculture income implying that the issue has been a subject of debate for about a century now. The report states that “there is no historical or theoretical justification for the continued exemption from the income tax of income derived from agriculture. There are, however, administrative, and political objections to the removal of the exemption at the present time.” The Taxation Enquiry Commission in 1953-54 has also recommended levying a surcharge on agriculture as regards to the non-agricultural income of the assessees.

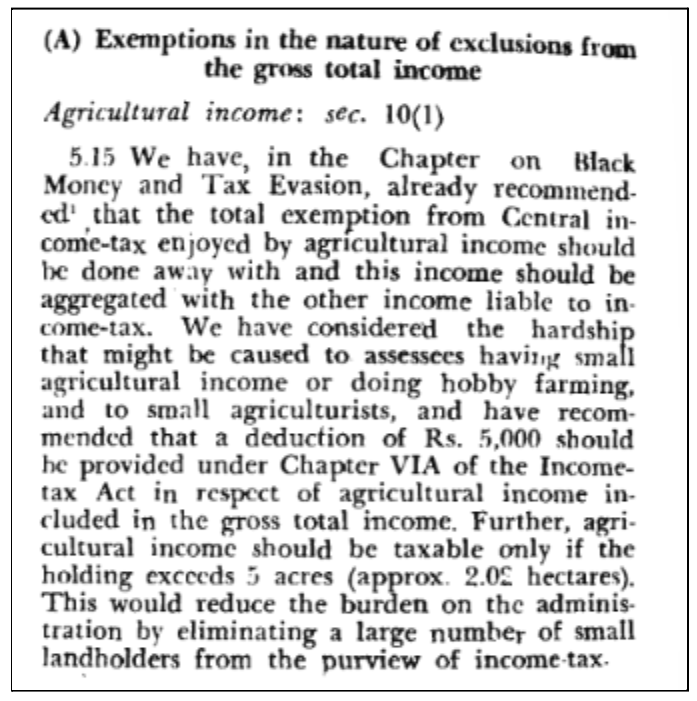

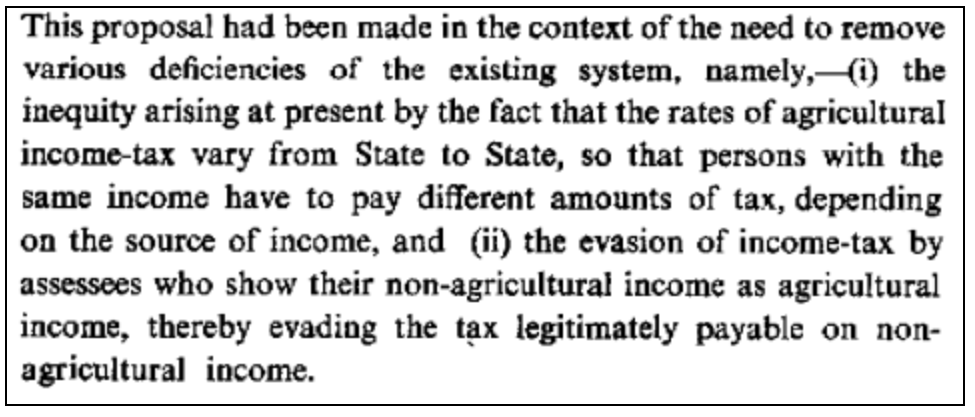

The Wanchoo Committee of 1971 on Direct Taxes suggested that the total exemption of agriculture income should be done away with and be aggregated with other income liable to income tax as the provision was being used for evading tax. It suggested that agricultural income should also be subject to a uniform tax on par with other income.

Tax evasion, money laundering, and inequity in taxation have also been highlighted

The opportunities offered by the exemption ‘for camouflaging black money’ have been mentioned in the Raj Committee on Taxation of Agricultural Wealth and Income report published in 1972, which suggests partial integration of agriculture income for taxing.

In 1972, the Law Commission of India prepared a report on the ‘Proposal for inclusion of agricultural income in the total income for the purpose of determining the rate of tax under the Income Tax Act, 1961.’ While preparing the report, the evasion of income tax by assessees by showing their non-agricultural income as agricultural income has been stated as one of the deficiencies of the income tax system.

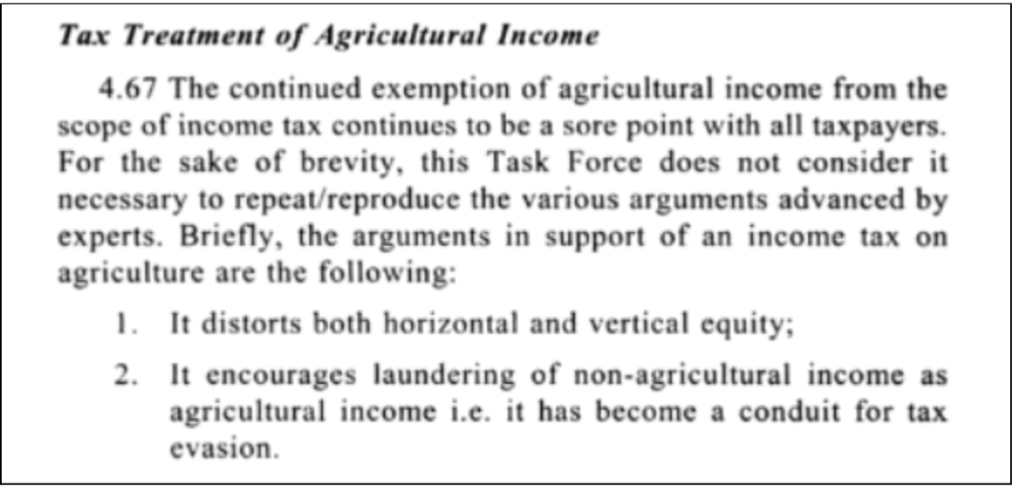

The Kelkar Committee Report on Tax Reforms in 2002 stated that the exemption to agriculture income is a distortion to both horizontal and vertical equity and encourages laundering of non-agricultural income as agricultural income.

Exemption has resulted in leakage to the tune of crores in revenues annually

The third Tax Administration Reform Commission (TARC) report of 2014 is among the recent reports that have detailed how the agricultural income of non-agriculturists is being increasingly used as a conduit to avoid tax and for laundering funds, resulting in leakage to the tune of crores in revenues annually. A solution suggested by the Commission was through taxing large farmers by setting income thresholds. It was on the basis of this report that the Comptroller and Auditor General of India (CAG) conducted an audit to ascertain the genuineness and correctness of the exemptions claimed for agricultural income in cases as granted by the Income Tax Department.

CAG Report brought to light the inefficiency in the IT Department’s functioning

The CAG report, published in 2019, studied a sample of 6,778 cases out of 22,195 scrutiny assessments carried out by the income tax department during 2014-15 to 2016-17, of those who had an agriculture income claim of more than Rs. 5 lakhs. The agricultural income of Rs. 3,656.25 crores were claimed in these 6,778 cases of which Rs. 2,544.21 crores were allowed. The CAG report observed that

- Exemption on agriculture was granted for 1,527 cases of those audited (22.5%) without adequate documentation or verification. The agriculture income allowed was worth about Rs. 500 crores in these cases. The proportion of cases was the highest in Maharashtra where the verification was inadequate in 303 (63%) of the 484 cases studied in the state, followed by Tamil Nadu (50%- 286 out of 565 cases) and Karnataka (45%- 229 out of 592 cases).

- No land records were available for 716 cases (10.6%) and proof of agriculture income such as ledger account, bills, invoices, etc. were absent for 1,270 cases (18.7%).

- Several errors in the computation were observed.

- Data entry errors were found in 36 cases, or 11% of the 327 cases for which records provided out of 2,746 cases that reported agricultural income of more than Rs. 1 crore. For the remaining cases where records were not provided, verification could not be done.

- Further, mistakes in levying interest, incorrect allowances of business expenditure, etc. were also observed.

The report noted that such lacunae in the system such as not verifying the expenditures would give way to bringing in black money/unaccounted money into the financial system under the garb of agricultural income. The CAG recommended that the income tax department should tighten its system in allowing exemption of income as agricultural income stating that the existing system is porous and open to misuse following its observations in the audit.

Corporates with hundreds of crores of profit are also exempted

Other private studies have noted how companies like Kaveri Seeds and Monsanto earned profits of Rs. 215.4 crores and Rs. 138.7 crores in 2014-15 were given exemptions for Rs. 186.6 crores and Rs. 94.4 crores respectively showing the inequity in the exemption. About 4 lakh people who declared agriculture income were granted exemption during 2013–14, with total agricultural income exempted from tax is Rs. 9,338 crores in the assessment period. Though the collection of tax on agriculture income is the state’s responsibility, even states have not considered this or failed to implement the legislations successfully. Uttar Pradesh introduced an agricultural income tax in 1948 which was repealed in 1957.

Public Accounts Committee stressed on strict compliance with procedures for verification of documents by IT Department

In April 2022, the Public Accounts Committee tabled a report in the Parliament on ‘Assessments relating to Agricultural Income’ in which the committee examined certain paragraphs of the CAG report which dealt with verification of documents for exemption, incorrect reflection in Income Tax Department’s database, and mistakes in assessments. The committee stressed on the need for strictly following the procedures for verification of documents for allowing exemptions.

The committee also recommended that all cases be individually checked where the agricultural income claim is above Rs. 10 lakhs noting that more than 21 lakh taxpayers claimed agricultural income in their 2020-21 returns and nearly 60,000 of them had reported agricultural income exceeding Rs. 10 lakhs. However, the Income Tax Department reported a shortage of manpower following which the committee asked the Ministry to come up with a mechanism for categorization of cases of agricultural income into three slabs- above Rs. 10 lakhs, Rs. 50 lakhs, and Rs. 1 crore in Computer Aided Scrutiny Selection (CASS) to target high evasion risk cases. The Committee also noted that a major chunk of agriculturists was reluctant to file income tax returns due to practical difficulties arising out of lack of awareness, frequency of going to IT offices and connectivity issues faced to travel to the Income Tax office.

Tax on Agricultural Income varies across countries

According to OECD, countries offer differential tax treatment for their agricultural sectors under their tax regimes. For instance, Finland and Denmark do not give any preferential treatment to farmers on personal income taxes whereas, in Korea, income from grains and other food crops are exempt from taxation while that from plant cultivation is tax-exempt if the revenue is less than KRW 1 billion. Countries like Latvia, Lithuania, and Norway have set income thresholds for granting exemptions.

Featured Image: Agricultural Income