As per the data provided by the government in Lok Sabha, the greatest credit amount under the ECLGS was disbursed by HDFC Bank as of September 2020. MSMEs from Maharashtra & Tamil Nadu are the biggest beneficiaries of the scheme. Here is a review of the scheme & associated numbers.

On 12 November 2020, Union Minister for Finance and Corporate Affairs made an announcement listing a series of measures under Aatmanirbhar Bharat 3.0. One of the announcements was regarding the Emergency Credit Line Guarantee Scheme (ECLGS), which has been extended until 31 March 2021.

Apart from extending the timeline, the scheme was also extended under this ECLGS 2.0 to include 26 stressed sectors impacted by COVID-19 including the Healthcare sector.

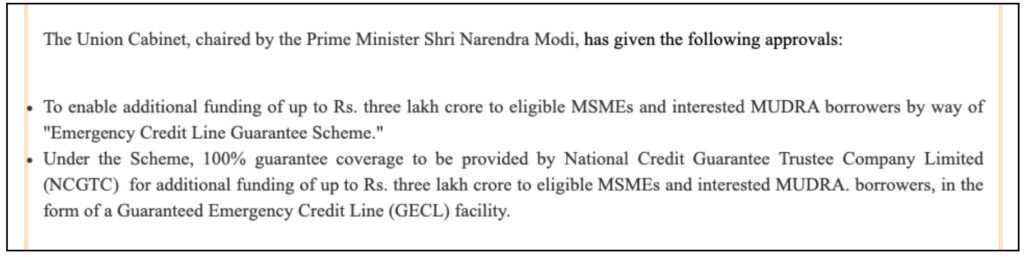

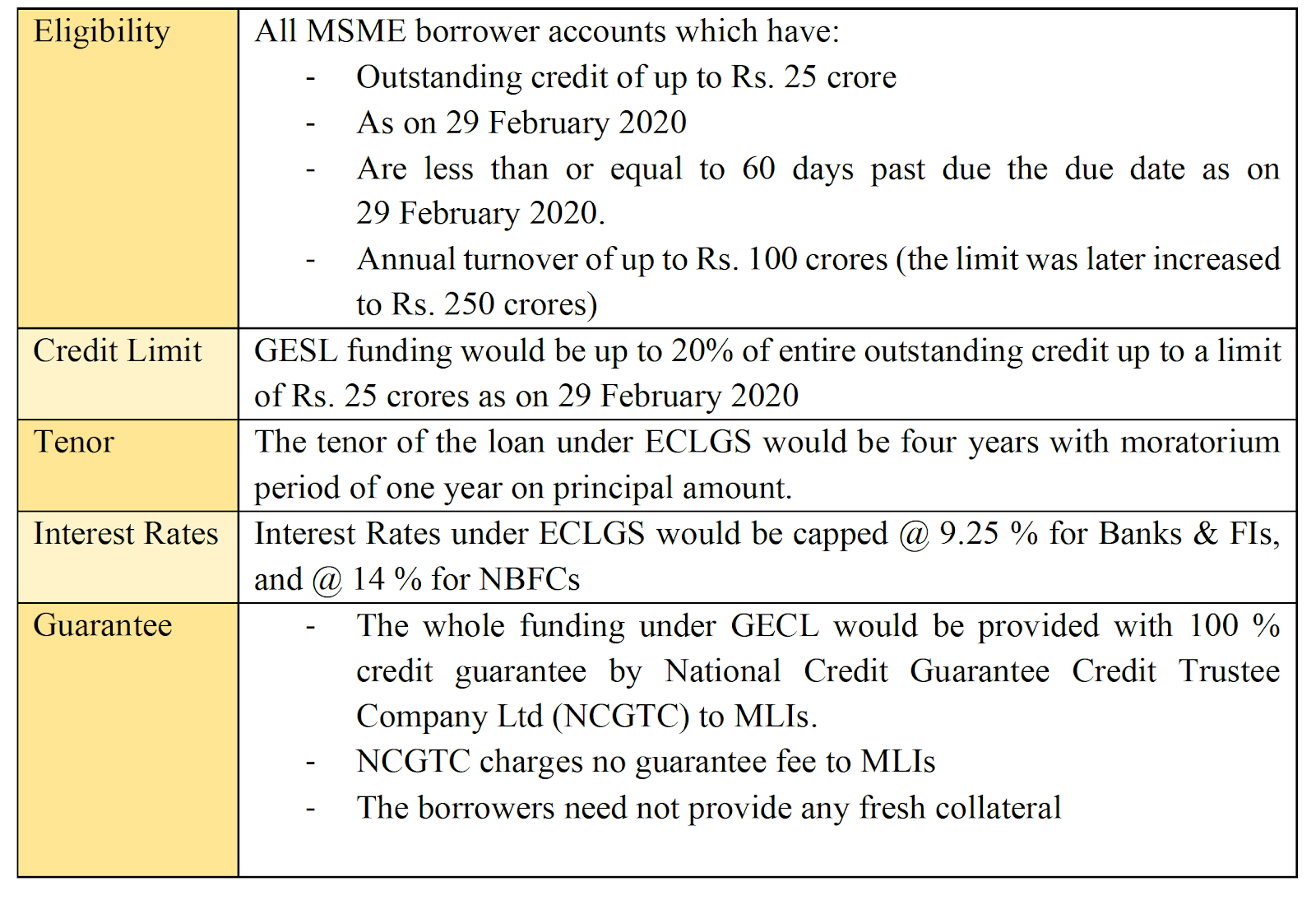

The scheme was initially announced as part of the Rs. 20 Lakh crore Aatmanirbhar Bharat package announced in May 2020 as part of COVID-19 relief measures. Under this scheme, collateral free automatic loans were extended to Businesses/MSMEs from Banks & NBFCs. As per the initial announcement, the scheme could be availed until 31 October 2020, which was later extended by one month to 30 November 2020.

ECLGS 2.0 removes the annual turnover capping limit on the businesses seeking loans

The situation created by the spread of COVID-19 and the subsequent lockdown has affected many businesses, especially MSMEs. Many of the business were cash strapped, rendering it difficult to continue or re-start the business.

The ECLGS was formulated in this context to mitigate the economic distress of these MSMEs by providing them with additional funding in the form of fully Guaranteed Emergency Credit Line (GECL). The government approved a funding of Rs. 3 lakh crores towards this scheme.

While the Government has set up a corpus of Rs. 41.6 thousand crores to be spread across three financial years, the main objective of the scheme is to provide an incentive to Member Lending Institutions (MLIs) i.e. Banks, NBFCs, Financial Institutions etc to enable availability of additional funding facility to MSME borrowers so that they can meet their operational liabilities. This scheme also focusses on mitigating the losses to Financial Institutions due to non-repayment of loans by these borrowers.

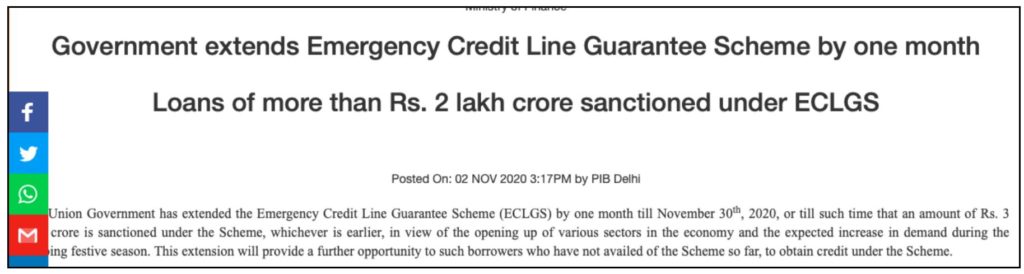

There is an upper limit of Rs. 3 lakh crores set for the loans being sanctioned under this scheme. This includes all the loans sanctioned under GECL from the date of announcement of the Scheme to 31 October 2020 or till an amount of Rs. 3 lakh crores are sanctioned under GECL, whichever is earlier. As per the update on 02 November 2020, a total of 2.03 lakh crores were sanctioned by 31 October 2020. Hence the cut-off was extended to 30 November 2020 or Rs. 3 lakh crores whichever is earlier.

ECLGS 2.0 made some changes to the existing scheme.

- ECLGS extended to 26 sectors identified by Kamath Committee including healthcare sector.

- Entities with outstanding credit of over Rs. 50 crores (not exceeding Rs.500 crore) as on 29 February 2020 and less than or equal to 30 days past due as on 29th February 2020 are eligible

- Loans under ECLGS 2.0 will have a 5-year tenor.

- There is no annual turnover ceiling for businesses to avail the loan facility.

- In line with this change, businesses which were ineligible due to Rs. 250 crore turnover limit can be now extended loan under ECLGS

- The time limit is extended to 31 March 2021 or lending of Rs. 3 lakh crores (both ECLGS 1.0 & 2.0), whichever is earlier.

Greatest amount of loans under ECLGS 1.0 was offered by HDFC followed by SBI

As highlighted earlier, one of the main purposes of this scheme is to encourage Lending Institutions to provide credit facilities for businesses/MSMEs who are under financial distress.

Responding to a question in Lok Sabha on 19 September 2020, the government provided the details of credit issued under this scheme.

As per the data provided by the government, as on 16 September 2020, a total of Rs.1.19 lakh crores were issued by various Lending Institutions. Among these, HDFC Bank Ltd has extended the highest amount of credit under this scheme with a total of Rs. 16.7 thousand crores. SBI & ICICI Bank Ltd complete the top three with Rs. 15.1 thousand crores and Rs. 9.3 thousand crores respectively. All the top 10 lenders are banks. In fact, there are only two Finance Institutes/NBFCs (Shriram Transport Finance Company Ltd & Tata Motors Finance Ltd.) in the Top 30 lending institutions by the total amount of credit under this scheme. The rest of them are banks.

Greatest amount of loans disbursed in Maharashtra

Top three states in terms of the greatest amount of credit disbursed under ECLGS are among the largest industrial/business states i.e. Maharashtra, Tamil Nadu & Gujarat. As per the information provided in Lok Sabha, as on 16 September 2020, a total of around Rs. 14.36 thousand crores worth of loans were disbursed in Maharashtra. Maharashtra & Tamil Nadu are coincidentally the states which also are among the ones with highest number of COVID-19 cases.

It has to be noted that this information is as on 16 September 2020, for the total credit disbursal of Rs. 1.19 lakh crores. However, as per the update on 02 November 2020, a total of Rs. 1.48 lakh crores have been disbursed out of the sanctioned Rs. 2.03 lakh crores to around 60.67 lakh borrowers.

A study notes the scheme helped in short term liquidity but there is inequitable distribution

On 16 September 2020, a Study on impact of ECLGS was submitted by National Institute of Bank Management for NCGTC. An earlier Impact Assessment report was published on 26 August 2020. As per the survey conducted across 1948 firms (including MSME & business enterprises), it was observed that :

- Most respondents felt that ECLGS will help in easing short-term liquidity problems.

- A smaller fraction feels that the ECLGS can help in increasing the business volumes, a longer-term benefit.

- GECL was mostly used for clearing supplier dues and to restart operations.

Many of the respondents acknowledged that it was an easy process for them to avail the loans from Banks & Financial Institutions.

However, few concerns have also been highlighted as part of the assessment study:

- Inequitable disbursement in distribution of GECL with 80% of the borrowers getting only 30% of the total disbursed amount.

- More than a third of the smallest borrowers did not get pre-approved loans and even the utilization is less since the amounts are small and do not meet the requirement of aiding business liquidity or growth.

- The study observes that the utilization is lower in West & East zones which are also the worst affected.

- Although the interest rates are lower in Public Sector banks, even the utilization rate is lower among them compared to others.

Featured Image: Emergency Credit Line Guarantee Scheme