Following the Supreme Court’s directions in February 2021, the RBI recently issued revised instructions to banks regarding the Safe Deposit Lockers. The new set of instructions are comprehensive and supersede the 2007 instructions. Here is a review.

Following the Supreme Court’s order in February 2021, the Reserve Bank of India (RBI) issued revised instructions on 18 August 2021, regarding safe deposit locker and safe custody article facility provided by banks. These instructions shall come into force with effect from 2022. The new guidelines have been issued taking into consideration the various developments in banking and technology, the nature of consumer grievances and the feedback received from banks and the Indian Banks’ Association (IBA). The rules will be applicable to both new and existing safe deposit lockers and the safe custody of articles facility with the banks.

In February 2021, the SC directed RBI to issue regulations concerning locker facility management

In Amitabha Dasgupta Vs. United Bank of India, the Supreme Court bench, on 19 February 2021, directed the RBI (RBI) to lay down regulations within six months mandating the steps to be taken by banks with respect to locker facility and safe deposit facility management. The bench expressed how the rapid advent of technology resulted in the transition from dual key-operated lockers to electronically operated lockers. It noted the possibility that miscreants may manipulate the technologies used in these systems to gain access to the lockers without the customers’ knowledge or consent and the customer is completely at the mercy of bank. In view of this, the SC bench asked RBI to issue regulations and rules with respect to the responsibility owed by banks for any loss or damage to the contents of the locker.

The revised instructions have been issued superseding the circular on the same issue issued by the RBI in 2007. The latest set of instructions are more comprehensive and detailed, unlike the erstwhile norms which were more generic. Further, the new norms also lay down guidelines pertaining to the use of technology. We explore some of the major issues addressed by the new set of instructions in this story.

Allotment of lockers

Existing customers of a bank and those customers who do not have a banking relationship with the bank who are in full compliance with the criteria under Know Your Customer (KYC) Directions may be given the safe deposit locker facility. Banks should carry out due diligence for all the customers who have applied for a locker. The due diligence shall be carried out for all the customers irrespective of their risk category, in contrast to the 2007 norms.

A branch-wise list of vacant lockers as well as a waitlist in Core Banking System (CBS) or any other computerized system compliant with Cyber Security Framework issued by RBI should be maintained by banks for allotment of lockers and transparency must be ensured in the process. All applications received for allotment of locker should be acknowledged and given a waitlist number, as mentioned in the erstwhile 2007 guidelines.

Locker Agreement

Banks must adopt a model locker agreement to be framed by IBA (Indian Banks Association) and ensure that any unfair terms or conditions are not incorporated in their locker agreements. The locker agreements with existing locker customers should be renewed by 2023. Banks have been asked to incorporate a clause in the locker agreement that the locker-hirer/s shall not keep anything illegal or any hazardous substance in the Safe Deposit locker. In case a bank has suspicions about the deposit of illegal or hazardous substances in the locker by a customer, banks can take appropriate action against the customer. A duplicate copy of the agreement entered on a duly stamped paper signed by both the parties must be provided to the customer to inform them of their rights and responsibilities while the original agreement is retained with the bank.

Locker Rent

To ensure prompt payment of locker rent, banks are permitted to take a ‘Term Deposit’, at the time of allotment of the locker. The ‘Term Deposit’ would cover three years’ rent and the charges for breaking open the locker in case of such eventuality. Banks cannot insist on ‘Term Deposits’ from the existing locker holders or those who have a satisfactory operative account. A proportionate amount of rent collected in advance must be refunded to the customer when they surrender the locker key. In the 2007 norms, the deposit was referred to as Fixed Deposit. Apart from this, no change in the regulation has been made.

In case of merger/closure/shifting of the branch which requires physical relocation of the lockers, the bank should give public notice in two newspapers including a local daily in vernacular language. The customers should be informed at least two months in advance and be given options to change or close the facility. However, in case of unplanned shifting due to natural calamities or any emergency, banks should try to intimate their customers at the earliest.

Security of the Locker

While the earlier norms briefly touched upon the security measures, the latest guidelines provide detailed guidance. It advises banks to conduct a risk assessment of ‘accessibility to locker without the customer’. It specifies the installation of CCTVs and ‘Access Control Systems’ for stronger security. The recordings of the CCTV camera should be preserved for 180 days.

With respect to accessing the locker, banks should send an email and SMS alert to the registered email ID and mobile number of the customer before the end of the day as a positive confirmation intimating the date and time of the locker operation and the redressal mechanism available in case of unauthorized locker access. Also, the custodian of the locker room should carry out a physical check of the locker room at the end of the day to ensure that lockers are properly closed and that no person is trapped in the locker room after banking hours

Settlement of Claims

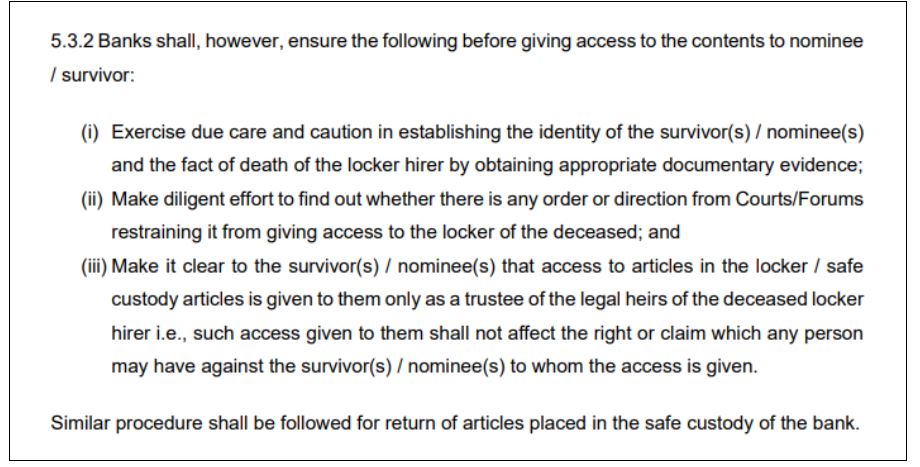

While the procedure for nomination and settlement of claims continues to remain the same, the new norms have mandated that settlement of claims in case of death of customer should take place within 15 days from receipt of claim and submission of requisite documents. The details of claims should be reported to the Customer Service Committee which shall review the claims.

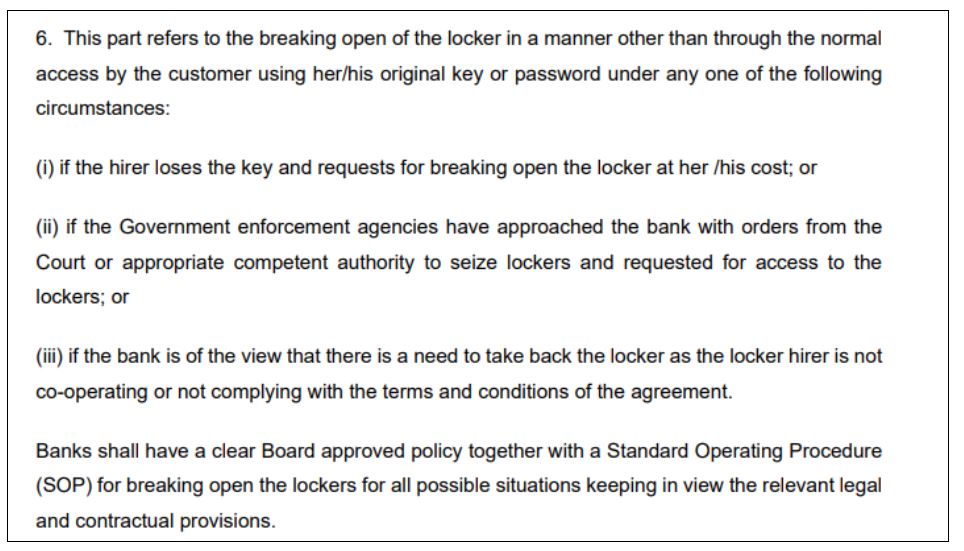

The revised norms clearly specify the circumstances under which the locker can be broken open. Earlier, banks were asked to have a clear procedure drawn up. If the locker remains inoperative for a period of seven years and the locker-hirer cannot be located, even if rent is being paid regularly, the bank can transfer the contents of the locker to their nominees/legal heir or dispose of the articles in a transparent manner.

Compensation and Liability of Banks

The responsibility of the bank in this aspect includes ensuring proper functioning of the locker system, guarding against unauthorized access to the lockers and providing appropriate safeguards against theft and robbery. Banks should abide by the ‘Master Directions on Frauds’ for reporting requirements about the instances of robberies, dacoities, thefts and burglaries.

Further, Banks are not liable for any damage or loss of contents of locker arising from natural calamities or ‘Acts of God’ like earthquake, floods, lightning and thunderstorm or any act that is attributable to the sole fault or negligence of the customer. However, banks should take measures to protect the area from catastrophes. On the other hand, the liability of the bank has been limited to 100 times its annual rent in case of fire, theft, frauds by employees, or building collapse. Banks should not offer any insurance product to their locker hirers for insurance of locker contents.

Exclusive data on theft/robbery from bank lockers is not maintained by RBI

According to a parliament response in August 2018, between 01 April 2015 and 31 July 2018, a total of 43 cases of theft took place in the lockers of Public Sector Banks (PSBs). the approximate amount of loss for customers was Rs. 16.8 crores. According to another response in August 2021, the number of cases of dacoity and theft from lockers in branches of nationalized banks had decreased from five cases reported during 2018-19 to one case each reported during 2019-20 and 2020-21. However, responses also state that the RBI does not maintain data on robberies in the bank lockers exclusively. However, Banks report all instances of theft/burglaries/dacoity/robberies to RBI which includes robbery/theft in branches, ATMs, theft from bank lockers etc.

Locker services are also provided by the private sector

As per the provisions of the Banking Regulation Act, 1949, a private banking company may engage in providing safe deposit vaults. The above discussed revised norms are applicable to all Scheduled Commercial Banks (including RRBs), Co-operative Banks, Small Finance Banks, Payments Banks, and Local Area Banks. In other words, these guidelines would also be applicable to private sector banks.

As per a 2019 Lok Sabha response, the Income Tax Department made seizures of black money worth Rs. 762 crores in 2014-15, Rs. 712 crores in 2015-16, Rs. 1,470 crores in 2016-17, and Rs. 993 crores in 2017-18 from bank lockers.

Featured Image: Safe Deposit Lockers,