The amount of foreign contributions received under FCRA has been steadily increasing though there has been a slight dip in recent years. Over Rs. 1.73 lakh crores of foreign donations were received between 2006-07 and 2018-19. Few states have received the bulk of these donations.

In this article, we briefly look at some of the important definitions and processes under Foreign Contribution (Regulation) Act (FCRA) and analyse the trends in Foreign Contribution received under the Act for the period 2006-07 to 2018-19.

The flow of foreign contribution to India is currently regulated under Foreign Contribution (Regulation) Act, 2010 read with other notifications/orders, etc., as issued from time to time, along with the recent amendments introduced by the Foreign Contribution (Regulation) Amendment Bill, 2020. The Foreign Contribution (Regulation) Act was first enacted in 1976.

In our earlier article, we looked at the major amendments to the FCRA and the changes brought about by the amendments in 2010 and 2020. We also analysed the trend in the cancellation of FCRA registrations from 20011 to 2019.

With respect to the regulation of foreign contribution to non-profit organisations, the 1976 Act allowed non-profit organisations to receive foreign donations freely, although they were required to annually report the amount received and spent. In 1984, the law was amended to make it mandatory for non-profit organisations to register before receiving any foreign donations. In 2010, the 1976 Act was repealed and replaced by the Foreign Contribution (Regulation) Act, 2010 where FCRA registration (which was a permanent registration earlier) became valid for a period of five years and must be renewed thereafter. With respect to the renewal process every five years, the 2020 amendments also add that the Central Government can initiate a fresh inquiry into the workings of the applicant before renewing the registration.

What is Foreign Contribution?

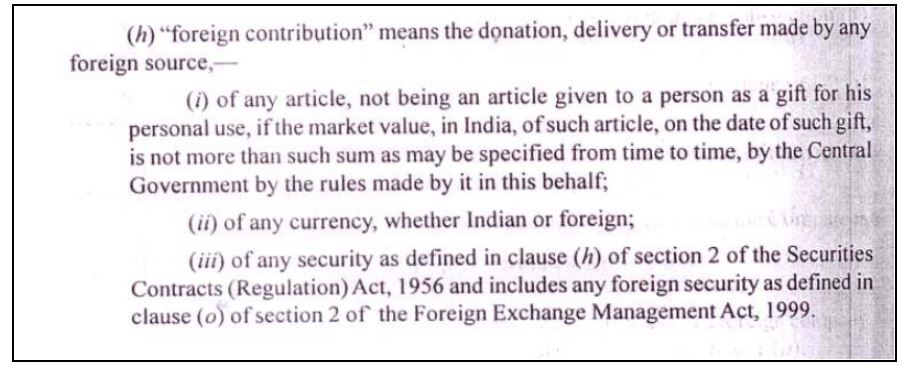

As defined in Section 2(1)(h) of FCRA, 2010, “foreign contribution” means a donation, delivery, or transfer of any article, currency, or foreign security from any foreign source, either directly or through one or more persons.

The interest accrued on the foreign contribution deposited in any bank or any other income derived from the foreign contribution is also be deemed to be a foreign contribution. However, any amount received by any person from any foreign source in lieu of goods & services rendered during the course of business is excluded from the definition of ‘foreign contribution’. What it means is that for-profit organizations receiving foreign money for goods or services rendered need not register and are not bound by this act.

What is a Foreign Source?

As defined in Section 2(1) (j) of FCRA, 2010, a foreign source includes:

- Government of any foreign country or territory and any agency of such Government.

- Any international agency, not being the United Nations or any of its specialized agencies.

- A foreign company.

- A corporation, not being a foreign company, incorporated in a foreign country or territory.

- A multi-national corporation referred to in section 2(g)(iv) of the Act.

- A trade union in any foreign country or territory, whether or not registered in such foreign country or territory.

- A foreign trust or a foreign foundation.

- A society, club, or other association or individuals formed or registered outside India.

- A citizen of a foreign country.

- A company within the meaning of the Companies Act, 1956, where more than one-half of the nominal value of its share capital is held, either singly or in the aggregate by any abovementioned entities.

Who can receive foreign contributions?

For an entity to receive a foreign contribution, it must fulfill the following conditions:

- It must have a definite cultural, economic, educational, religious, or social programme.

- It must obtain the FCRA registration/prior permission from the Central Government.

- It must not be prohibited under the Act.

FCRA 2010 and its subsequent amendments prohibits certain individuals and organisations from accepting any foreign contribution, which includes government employees, print or visual media outlets, and so on.

Registration, Prior Permission, Renewal and Filing of Returns under FCRA

There are two modes of obtaining permission to accept foreign contributions: i) Registration ii) Prior Permission. Under the 2010 Act, FCRA registration is valid for five years and must be renewed thereafter, whereas under the 1976 Act it was a permanent registration. Any application for a grant of registration or prior permission is to be submitted on the FCRA Online Portal. Specific instructions and the list of required documents to be uploaded are available on the portal.

For grant of registration under FCRA, the association should meet the following criteria:

- Registered under an existing statute like the Societies Registration Act, 1860 or the Indian Trusts Act, 1882 or section 25 of the Companies Act, 1956 (now Section8 of Companies Act, 2013), etc.

- In existence for at least three years and has undertaken reasonable activity in its chosen field for the benefit of society.

As mentioned above, an organization in the formative stage is not eligible for a certificate of registration. However, such organizations can apply for a grant of prior permission for receipt of a specific amount from specific donor/donors for carrying out specific activities/projects. For this purpose, the association should meet the following criteria:

- Registered under an existing statute like the Societies Registration Act, 1860, etc.

- Submit a commitment letter from the donor indicating the amount of foreign contribution and purpose.

- For Indian recipient organizations and foreign donor organizations having common members, FCRA Prior Permission is granted to the Indian recipient organizations subject to its satisfying the following:

- The Chief functionary of the recipient Indian organization should not be a part of the donor organization.

- At least 75% of the office-bearers/ members of the Governing body of the Indian recipient organization should not be members/employees of the foreign donor organization.

- In the case of a foreign donor organization being a single person/individual that person should not be the Chief Functionary or office bearer of the recipient Indian organization.

- In the case of a single foreign donor, at least 75% of office bearers/members of the governing body of the recipient organization should not be the family members and close relatives of the donor.

With respect to the renewal of registration, associations are to apply on the FCRA Online Portal within 6 months of the expiry of their existing registration certificate.

With respect to the filing of annual returns, associations are to file the return on the FCRA Online Portal for every financial year (01 April to 31 March) within a period of nine months from the closure of the year i.e., by 31st December each year, duly accompanied by balance sheet and statement of receipt and payment.

An association not filing annual return on time may face the following consequences:

- The imposition of a penalty for late submission of return.

- Cancellation of registration.

- Prosecution for violation of provisions of FCRA, 2010.

For registration, the association is required to pay a fee of Rs. 10,000 and for prior permission, the fee is Rs. 5,000 and for renewal, the fee is Rs 5000.

For all FCRA services provided through the online portal, the Aadhar number of all its office bearers, directors, and/or key functionaries and Unique ID from Darpan Portal are mandatory now. The Darpan Portal facilitates NGOs to obtain a system-generated Unique ID, which is now mandatory to apply for grants under various schemes of Ministries, Departments, and Governments Bodies.

Foreign Contributions under FCRA have increased over the last 13 years

With the data available on the FCRA Online Portal, we analyse the trends in Foreign Contribution received under the Act for the period 2006-07 to 2018-19.

Please note: (i) We have not included the year 2019-20 because the process of filing returns is not complete and hence, the amount of donations received is not final. (ii) The figures are based on total annual returns filed by registered organisations on the FCRA Online Portal for the given period and may not necessarily represent the total quantum of foreign donations.

The quantum of foreign contribution shows an overall rising trend over the period 2006-07 to 2019-20. The highest amount of Foreign Contribution amounting to Rs. 17,671 crores were received in 2015-16. After the year 2015-16, the amount of foreign contribution has fallen but it is still higher than the years preceding 2015-16.

From 2006-07 to 2018-19, roughly speaking, the quantum of contributions received under FCRA increased by almost half of the initial amount.

What about State-wise donations?

In order to understand the state-wise distribution of foreign contributions under FCRA, we will look at:

- A heat map indicating the state-wise distribution and variation of overall foreign contribution for the period 2006-07 to 2018-19.

- A grid chart indicating the year-wise growth in the foreign contribution for major states.

While a non-profit organisation might be registered in one particular state, it is possible that the scope of its work might be extended beyond that state. However, since the annual return filings only indicate the state of registration, these figures only represent the quantum of foreign contributions received by each state vis-à-vis its registered organisations under FCRA and do not bear any indication on the subsequent utilisation of the fund geographically or otherwise.

The following map shows a significant variation in the amount of foreign contribution received across the country. For the overall periods from 2006-07 to 2018-19, the following can be observed:

- The highest amount of foreign contribution was received by Delhi at Rs. 37, 213 crores, followed by Tamil Nadu at Rs. 24, 271 crores, Karnataka at Rs. 17,802 crores, Maharashtra at Rs. 17,064 crores, Kerala at Rs. 13,870 crores, Andhra Pradesh at Rs. 11,300 crores, etc.

- Southern states account for a majority of the total foreign contributions received for the periods 2006-07 to 2018-19. To be precise, the states of Andhra Pradesh, Karnataka, Kerala, Tamil Nadu, and Telangana received 43.5% of the total foreign contributions from 2006-07 to 2018-19.

- Northern states, except for Delhi and the central state of Maharashtra, have received comparatively low proportions of foreign contribution.

- North-eastern states have received the lowest shares of foreign contribution.

Let’s also take a look at the year-wise distribution of foreign contribution received by different states for the period 2006-06 to 2018-19.

- The year-wise trends also show a significant variation in the number of foreign contributions received across the country for each succeeding year.

- Most states have received the highest contribution in the year 2015-16, after which the contributions have fallen but it is still higher than the years preceding 2015-16.

- We can clearly see that Delhi, southern states, and Maharashtra have consistently received higher amounts of foreign contributions whereas other states have consistently received extremely low to negligible amounts of contributions over the years.

- The pattern of foreign contributions being concentrated in a limited number of states is evident for over a decade.

In a nutshell, the quantum of foreign donations under the Foreign Contribution (Regulation) Act has been steadily rising over the years. The majority of the foreign donations have been consistently received by registered organisations in a few particular states such as being Delhi, Tamil Nadu, Karnataka, Maharashtra, Kerala, and Andhra Pradesh.

Featured Image: Foreign Contribution (Regulation) Act (FCRA)