[orc]The RBI has amended the Banking Ombudsman scheme to include additional issues as grounds for a complaint. The number of complaints is set to increase with these changes.

The Reserve Bank of India (RBI) has recently amended the Banking Ombudsman Scheme to include complaints relating to Misselling, Mobile/Electronic Banking. With the inclusion of these issues, the complaints to the Banking Ombudsman are set to increase. In 2015-16, more than 90000 complaints were received by the Banking Ombudsman across the country.

What is Banking Ombudsman Scheme?

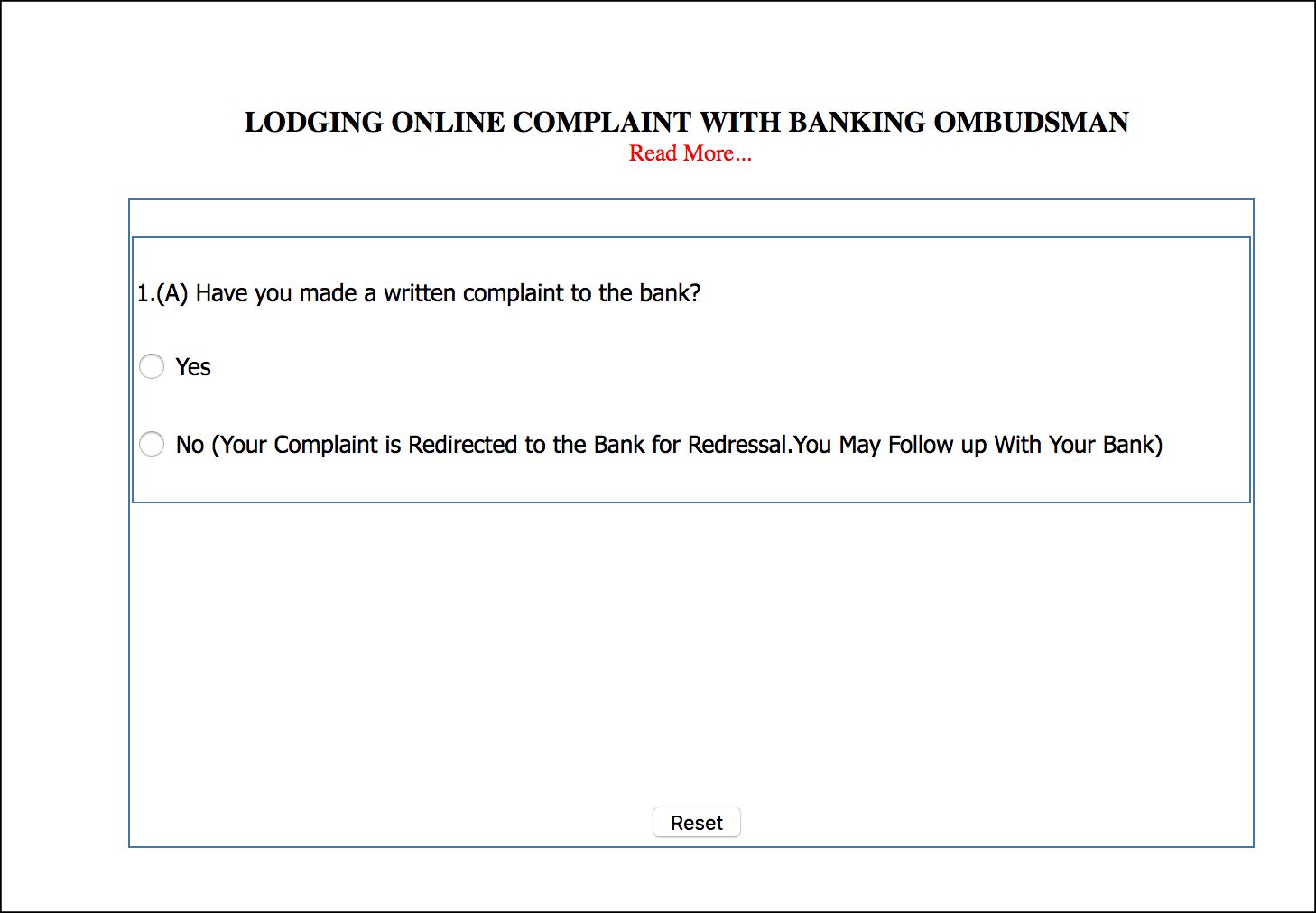

The Banking Ombudsman scheme was introduced in 2006 to enable resolution of complaints in case of certain services rendered by banks and to facilitate the satisfaction or settlement of such complaints. Before approaching the Ombudsman, the complainant has to make a written representation to the bank. If the bank has rejected the complaint or has not responded within one month, then a complaint can be lodged with the Ombudsman.

What kind of issues are covered by the Banking Ombudsman Scheme?

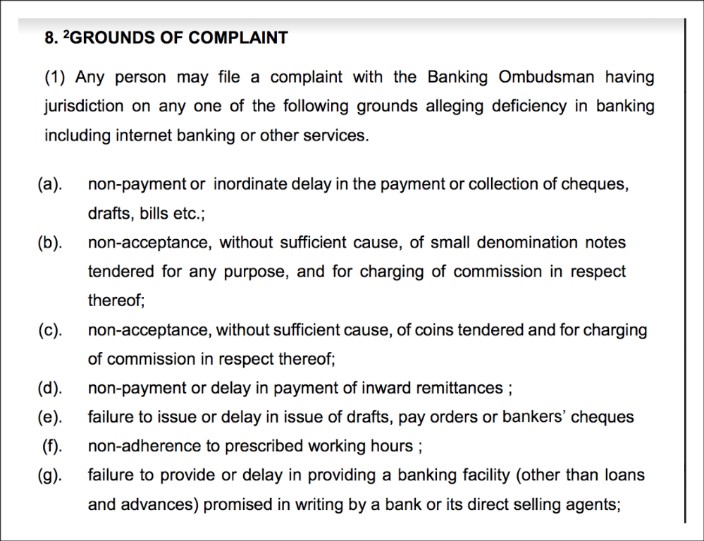

The grounds for complaint are well defined in the scheme document. A complaint can be made on one of the following grounds

- Non-payment or inordinate delay in the payment or collection of cheques, drafts, bills etc.

- Non-acceptance, without sufficient cause, of small denomination notes tendered for any purpose, and for charging of commission

- Non-acceptance, without sufficient cause, of coins tendered and for charging of commission

- Non-payment or delay in payment of inward remittances

- Failure to issue or delay in issue of drafts, pay orders or bankers’ cheques

- Non-adherence to prescribed working hours

- Failure to provide or delay in providing a banking facility (other than loans and advances) promised in writing by a bank or its direct selling agents

- Complaints from Non-Resident Indians having accounts in India in relation to their remittances from abroad, deposits and other bank- related matters

- Refusal to open deposit accounts without any valid reason for refusal

- Levying of charges without adequate prior notice to the customer

With the recent amendment, the RBI has included the following as possible grounds for a complaint.

- Non-adherence to the instructions of Reserve Bank on ATM / Debit Card and Prepaid Card operations in India

- Account debited but cash not dispensed by ATMs

- Account debited more than once for one withdrawal in ATMs or for POS transaction

- Less/Excess amount of cash dispensed by ATMs

- Debit in account without use of the card or details of the card

- Use of stolen/cloned cards

- Non-adherence by the bank or its subsidiaries to the instructions of Reserve Bank on credit card operations

- Unsolicited calls for Add-on Cards, insurance for cards etc.

- Charging of Annual Fees on Cards issued free for life

- Wrong Billing/Wrong Debits

- Threatening calls/ inappropriate approach of recovery by recovery agents including non-observance of RBI guidelines on engagement of recovery agents

- Wrong reporting of credit information to Credit Information Bureau

- Delay or failure to review and correct the credit status on account of wrongly reported credit information to Credit Information Bureau.

- Non-adherence to the instructions of Reserve Bank with regard to Mobile Banking / Electronic Banking service in India by the

- Delay or failure to effect online payment / Fund Transfer

- Unauthorized electronic payment / Fund Transfer

With these new inclusions, the scope has widened and the number of complaints is set to increase in the coming years.

How does one file a complaint with the Banking Ombudsman?

A complaint can be lodged with any of the 20 Banking Ombudsman offices based on the jurisdiction of the bank. The complaint can be filed online or offline. Relevant documentary proof has to be enclosed to support the claims. The Ombudsman may also call for additional documentation if required. It is advisable that a complainant go through the compendium of cases handled by the various Banking Ombudsman offices in the past to get an idea of the kind of cases dealt by the Ombudsman.

The Ombudsman can pass an award directing payment of compensation. The amount of compensation cannot be more than the actual loss suffered by the complainant or Rs 20 lakh, whichever is lower. The compensation awarded will be exclusive of the amount involved in the dispute. The Ombudsman can also award compensation in addition to the above to the tune of Rs 1 lakh taking into account the loss of the complainant’s time, expenses incurred by the complainant, harassment and mental agony suffered by the complainant.